© wallstreet-online.de

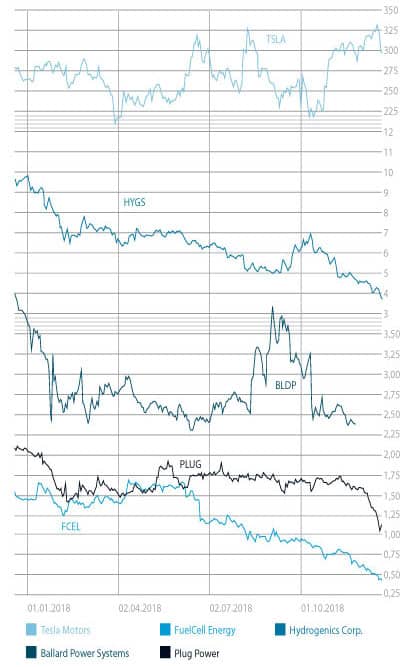

Hydrogenics (Nasdaq: HYGS) seems to be facing similar headwinds in China, mostly with regard to funding, bid requests and grant approval. It said the country offered excellent prospects; everything was just moving along a bit more slowly than expected. At the very least, backlog at Hydrogenics added up to USD 132 million, more than half of which originates with Alstom contracts for fuel cell trains. Thirty trains have already been ordered and more are said to follow this year. The company had also submitted bids for projects with a total contract value of more than USD 100 million. In Norway, it won a contract for installing a 2.5-megawatt system that is to store electricity generated by a 45-megawatt wind farm. In Germany, it was chosen to construct a power-to-gas system in Wuppertal.

Third-quarter results weren’t up to standard, with the company posting a loss of USD 3.4 million, that is, minus USD 0.22 per share instead of minus USD 0.07, as expected, and revenues of USD 7.7 million. High fluctuations between quarters were the norm, company management said, considering FuelCell Energy carried out projects with multi-quarter deliveries. None of it, however, would influence long-term outlook, since interest in fuel cell technology was on the rise and Hydrogenics had strong, diversified product platforms, valuable patents and the expertise needed to make it in the industry.

A quick look at Weichai’s strategy (see Good and Bad News from Ballard Power) suggests that, in theory, companies will soon want to branch out into other areas by buying into businesses that produce electrolyzers or fueling stations. If my prediction comes true, Hydrogenics could be a candidate for this kind of acquisition. Take Nikola Motors for example: Not only is it planning to sell fuel cell trucks, but it also has partners build hydrogen fueling stations and has been ordering electrolyzers from Nel Asa. Toyota has been doing the same, building power plants in partnership with FuelCell Energy to produce hydrogen for its vehicles and setting up fueling stations in partnership with energy suppliers.

The lack of stations is a challenge that manufacturers have begun to address themselves without waiting on gas station managers to add hydrogen pumps, which they probably won’t do until they see enough fuel cell cars on the road. Now, all of the above benefits Hydrogenics. Its stock price, lowered by third-quarter results, presents another opportunity to buy shares, provided shareholders see the small-cap company as having the outlook I described and are considering investing long term.

Risk warning

Share trading can result in a total loss of your investment. Consider spreading the risk as a sensible precaution. The fuel cell companies mentioned in this article are small and mid-cap ones, i.e., they may experience high stock volatility. This article is not to be taken as a recommendation of what shares to buy or sell – it comes without any explicit or implicit guarantee or warranty. All information is based on publicly available sources and the content of this article reflects the author’s opinion only. This article focuses on mid-term and long-term prospects and not short-term profit. The author may own shares in any of the companies mentioned in it.

Written by Sven Jösting

0 Comments