BMV Energy GmbH is entering the market as another player in hydrogen refueling stations. The owner-managed, medium-sized company together with Score founded H2Now GmbH in August 2023 and appointed Stefan Schwarzer as managing director to advance the establishment of refueling stations with green hydrogen, particularly for commercial vehicles. In November 2023, the Berlin-based company announced that the company will be co-represented with second managing director Andrew Stracke in April 2024. Stracke was prior to this a member of the executive board at Westfalen AG.

H2Now was brought to life jointly by the petroleum company BMV and Score, a gas station operator with headquarters in Emden, to bundle the synergies of the medium-sized companies. To the BMV corporation belongs a gas station network with 145 stations of the brands Sprint and Go. According to the management, there are “already established locations suitable for the addition of a hydrogen refueling station with the help of H2NOW, to become part of the Germany-wide hydrogen station network and be supported with extensive know-how in project planning, funding, realization and operation.”

In autumn 2023 as well, the Hydrogen Technology Expo was again the event you had to be at. For the third time in a row, the British organizer Trans-Global Events Ltd was able to dramatically increase the number of exhibitors as well as visitors – which is why the trade fair halls of the Hanseatic city on the Weser (Bremen) will no longer be sufficient in 2024. The move to Hamburg this year is therefore inevitable and had been predicted early on by H2-international (see H2-international Feb. 2023).

The trend is unmistakable: More and more companies from the mechanical engineering, electrical and chemical industries are flooding the hydrogen market. Accordingly, a large number of completely new exhibitors could be found in the four trade fair halls in Bremen. Among them were numerous unknown names, but also heavyweights such as Saudi Aramco, ExxonMobil or ITM Power.

Advertisements

After 180 exhibitors in the first and 350 in the second year, this time there were over 550 – in 2024, there should be at least 100 more. The number of visitors increased from 5,000 in the previous year to over 10,000.

Moving towards mass production

Companies like the chemicals corporation Gore had explicitly “chosen this trade show in Europe” because “Europe is furthest along.” Nouchine Humbert, Global Marketing Director of W.L. Gore, told H2-international, “This is a market where we expect strong growth.” Referred to is particularly the electrolysis sector, because in comparison fuel cells need “many more square meters than electrolyzers.”

Sufficient production capacity is available to the North American company – in Japan. The production lines there are enough for another five years, asserted Rainer Enggruber, director of the division PEM/water/electrolysis products. Gigawatt announcements are therefore not a challenge for the membrane manufacturer, it was confidently stated.

New tubular reactor

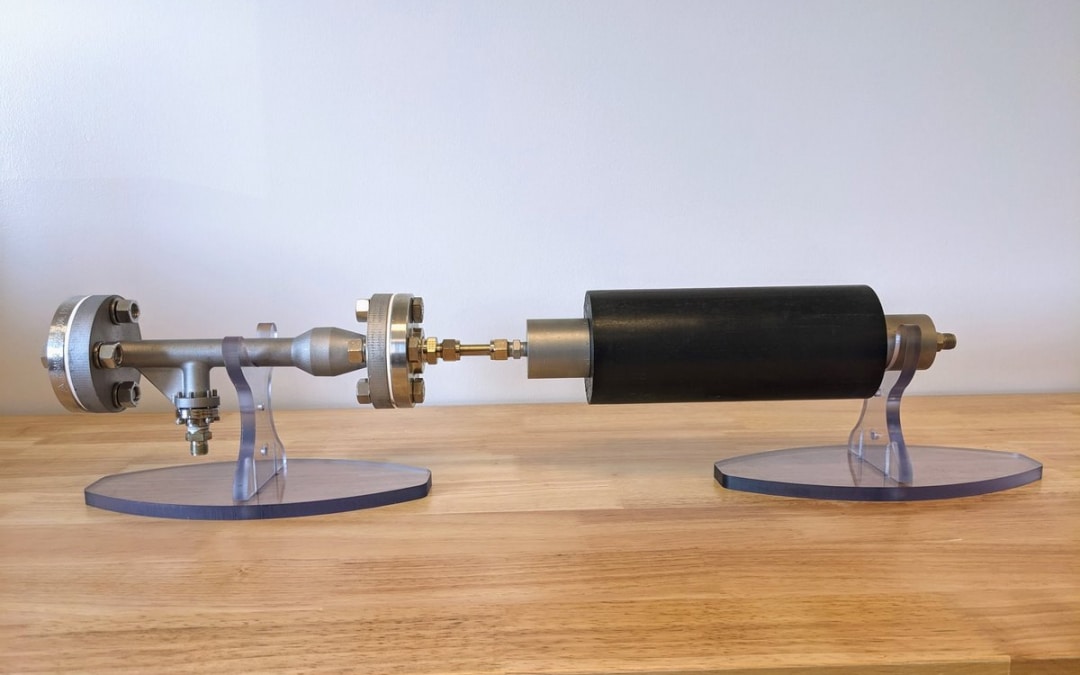

An innovation was shown by the Hebmüller Group. Sales director Marc Hebmüller presented the prototype of the HydroGenMHD (see Fig. 1), an H2 generation device from One Scientific of Johnson City, Tennessee. The company Hebmüller is the European licensee of the US system developer that developed this compact tubular catalyst, in whose magnetohydrodynamic chamber hydrogen is generated upon splitting off of oxygen from water vapor.

Marc Hebmüller explained: “This innovative technology employs a unique system where superheated steam is subjected to a catalyst and intense magnetic fields generated through the MHD process. These magnetic fields induce controlled plasma dynamics within the feedstock, facilitating the dissociation of molecules into hydrogen gas and oxygen gas.”

Stack based on circuit boards

A completely new concept for the production of fuel cells was presented by Bramble Energy: a fuel cell stack based on printed circuit board technology. The British company founded in 2017 relies here on the plastic FR4, which provides the necessary stability, and copper as a heat as well as electricity conductor. Between two circuit boards is one membrane each, which means that bipolar plates can be dispensed with entirely. Instead, a monopolar plate constitutes a single cell, of which several are then stacked.

The technology readiness level Carsten Pohlmann, director for business development (see Fig. 2), puts at TRL 9, and the price per kilowatt at 100 USD. First tests in a Renault demonstrator and with a 100 kW system for a double-decker bus are already underway.

Carsten Pohlmann presented in Bremen for the first time the circuit board cell from Bramble

The next Hydrogen Technology Expo Europe will take place October 23 and 24, 2024 on the fairgrounds of Messe Hamburg. It therefore will overlap by one day with WindEnergy.

The share price of Weichai Power has risen by almost 50 percent in the last few weeks. The reason is the partnership with BYD in the electrification of large vehicle fleets. A perfect joint venture, it seems. Weichai Power with BYD could – my guess – be pushing the door open to fuel cells, since alongside battery-electric trucks and other commercial vehicles, the fuel cell is perfect for long-haul journeys.

Weichai has a joint venture with Ballard Power in China (51:49), with a capacity of already 20,000 FC modules per year. And Weichai will be one of the main beneficiaries when in China a large subsidy program for fuel cells and hydrogen comes – maybe 2024 or 2025. Weichai is China’s largest diesel engine manufacturer, which is now moving towards e-mobility – comparable with Cummins Engine in the USA. Weichai is also cooperating with Bosch.

Advertisements

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Short sellers are working massively against the company at the stock exchange. There were shortly even nearly 200 million shares sold short (on Nov. 16 still 193 million). But now, a price change upwards seems very likely. The reason could lie in the comments made at the press conference on the third quarter results, which Nikola – in my words – sees as being on the right track. The company amassed about 250 million USD in liquidity in the third quarter, and now has available 705 million USD in capital access.

The damage due to recalled battery-electric trucks was reported as 61.8 million USD (warranty reserve), where Nikola not only resolved this problem, but employed batteries from a still unnamed supplier that possessed advantages over the previous model, was the comment from the company. Additionally, the truck will be equipped with more features that will give the driver more options during use, for example from a distance using a smartphone app, the truck could be already prepared with heating in the winter and air conditioning in the summer, before the driver gets in. The battery-electric truck will, after the retrofitting in the first quarter, again find its way to customers.

Advertisements

Now orders can come

There are 277 letters of intent for the purchase of the hydrogen-powered truck. In the fourth quarter, 30 to 50 of them are to be delivered and between 11 and 19 million USD turnover generated. With the battery-electric truck, meanwhile – despite the recall – an individual order of 47 units will be gained. In the next two years, Nikola is determined to deliver on average 250 to 300 trucks of both types per quarter.

The cash burn is at 100 million USD in the quarter, where for the current quarter, the financial effects of the recall on the battery-electric truck are still to be felt (61.8 million USD, of which about 38 million USD is capital that will be used). And the better the scaling of the truck production goes, the more cost-effective they can be manufactured, in order to at the end of the day come out with a good profit margin. Consider this: Money is the future will be earned especially with electricity and hydrogen and not with e-trucks per se. Nikola is at the start of its (success) story.

California setting the pace

Nikola is concentrating, for good reason, on the US state California. Firstly, the best subsidies (up to around 408,000 USD per truck) are there; secondly, the time pressure for shippers to replace diesel-powered by CO2-free trucks is very high. Already starting 2024, in California only the last-mentioned will be allowed at port facilities, so there will be new registrations only for battery-electric or hydrogen trucks. We’re talking about over 30,000 trucks alone in this market segment – a winning pass for Nikola Motors, since in the Inflation Reduction Act are provided also 2.6 billion USD in subsidies specially for port facilities and also drayage trucks as well as for the H2 infrastructure.

Additionally, the competition for Nikola in this truck segment will be sparse for years to come. The look at the already approved vouchers for e-trucks is cause to celebrate: 96 percent of the vouchers of the California’s HVIP program for hydrogen-powered trucks and 50 percent of the vouchers for battery-electric trucks are attributable to Nikola. After all, Nikola is to have received approval of already over 400 vouchers for the two truck variants. A respectable success.

Lawsuit against Milton won

The lengthy legal dispute with company founder Trevor Milton was won. On October 20 came the decision. Milton must now pay 165 million USD to Nikola, which includes procedural costs Nikola first had to pay and now receives back. It should be noted here that there is still no indication of when the money will flow. Nikola still has to pay a portion to the SEC itself, as they reached a settlement of 125 million USD and must itself fulfill it. If 165 million USD flows from Milton soon, Nikola’s liquidity will rise, as the SEC payments will be divided over the next years.

Goals ambitious but realistic

Currently, Nikola can produce 2,400 trucks of either variant per year. In order to be profitable, sales of 1,000 trucks in 2024 and 1,500 in 2025 are needed. These targets are considered realistic from the company’s perspective, if Nikola delivers 250 to 300 truck per quarter. In my view, there will also be some large orders. Beyond this, declarations like the letter of intent (LoI) with Anheuser-Busch (800 trucks) will also flow into the orders on hand, is my expectation.

Nikola Motors – The Tesla of trucks?

For this hypothesis, I earned a lot of criticism. One cannot compare a startup like Nikola, though, with the success story of Tesla. One can say: Tesla started small, then came Elon Musk. The company reported heavy losses for many years and was even on the verge of bankruptcy before the breakthrough came. In the first three years, Tesla earned money, but not with the e-cars but with emission rights that could be sold to other car manufacturers. Tesla solved the chicken-and-egg problem by providing the electricity for the battery-electric vehicles itself by establishing a charging network made of its own Supercharger stations. Who would have bought a car from Tesla if there had been no charging option – as a package, even free of charge for years?

Nikola is doing the same – only for trucks with the help of electric charging stations and H2 refueling stations. Nikola wants to earn money with electricity and the self-produced or purchased hydrogen. In the USA are waving high subsidies of three USD per kg. Tesla continues to address the market for e-cars, but Nikola the segment for trucks. Both companies can be considered disruptive – they change markets and business models. Both are first movers.

Tesla and its CEO was met with much skepticism, but they proved that change is possible. Nikola is doing the same – only for commercial vehicles. Whether both can be compared with regard to the development of their valuation or share prices time will tell. For Nikola I am extremely optimistic.

Chief financial officer leaves the company

Stasy Pasterick was just six months in office as CFO. She is going over to Universal Hydrogen in the same capacity. It will be interesting to see who her successor will be.

Capital increase secures the company

On December 6, 2023, Nikola’s plan to raise fresh capital on the stock market became known. It entails a convertible bond of a nominal 175 million USD with 8.25-percent coupon (green bonds) with maturity December 2026 (0.90 USD conversion price per share) and 100 million USD in new shares at 0.75 USD per share. The share price fell from around 1 USD probably because – no guarantee – a hedging took place, so the price was depressed, as one can retain and stock up on the share after the capital raise. The share also fell because short sellers wanted to use the capital increase as a negative for themselves.

In accordance with experience, this measure will have already been successfully implemented by the time you read these lines. With it, Nikola is then thoroughly financed and will ultimately have 500 million USD in the bank. That the share price is rising above 1 USD again is also in the nature of things, because the financiers (investment banks such as Nomura) will most likely not accept a delisting of the share (it will come to this if the price sinks below 1 USD for a longer time).

Summary: Nikola is well on the way to positioning itself as a first mover in CO2-free trucks in the USA – first in California, later across the whole country and in parallel in Canada, where likewise large subsidy sums up to 380,000 CAD per truck are waving. Comprehensive funding programs are acting as a turbo, as the buyers of the trucks can comply with the regulatory pressure and are financially incentivized as well. The H2 infrastructure is being established by the company itself, but will be financially accompanied by business partners such as Voltera (EQT) and is receiving a boost by a 7-billion-USD program of the Biden administration, in which seven hydrogen hubs are to be established in the USA. The stock market will not be able to avoid newly valuing Nikola as a startup: In the right market at the right time. Maybe Nikola will even be the H2 share that develops the most price potential. What’s the phrase? No risk, no fun.

Nikola’s management team is considered excellent. CEO Stephen Girsky pointed out that this includes top managers who no longer actually have to work in a start-up, but who are happy to contribute their expertise to make the company’s vision a reality. This is the right approach – out of conviction and with experience.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

My recommendation to use the temporarily very weak prices in Cummins for continued and new buys has already paid off: The share price grew from around 200 to over 255 USD. And it will continue to, even though Cummins is increasingly focusing on new markets like hydrogen (engines, electrolysis, stacks for commercial vehicles, etc. – we reported).

Cummins can finance its own growth well from its own means through corporate earnings. On average, 34 percent of corporate profits are distributed to shareholders as dividends – in 2022, it was 6.28 USD per share. This was topped up by seven percent on July 11 to 1.68 USD per share for the quarter. The company’s growth rate of 26 percent per year on average over the past five years is solid. Cummins now sees turnover in the current fiscal year at 33 billion USD and expects an earnings per share of 19.80 USD, which corresponds to a growth of 31 percent. A good justification for further rising prices.

Advertisements

Share price decline despite good figures

Cummins reports for the second quarter a turnover of 8.6 billion USD (plus of 31 percent) and profit of 720 million USD, which came out lower than expected, however, and allowed the share price to sink from over 255 USD to 230 USD – thus already back to buy level, as the guidelines are unchanged.

Together with Air Liquide, Cummins Engine acquired Canadian company Hydrogenics in 2019 for 290 million USD. In the transaction, Air Liquide retained at that time a 19 percent share in the company. This share Air Liquide has now sold to Cummins for the equivalent of about 156.5 million USD, making the value of Hydrogenics as per today the equivalent of over 823.7 million USD. Cummins plans with subsidiary Accelera, in which Hydrogenics is consolidated, to build an annual electrolysis capacity of 3.5 GW in the next years. A diversity of large orders – 500 MW in China, 500 MW in the USA, 500 MW in Spain and 1 GW in Belgium – are already in the books of Cummins or Accelera.

Considering that Plug Power intends to build 5 GW of electrolysis capacity within a few years and is currently valued on the stock exchange with a good 6 billion USD, Cummins should consider placing its subsidiary on the stock exchange, possibly while also retaining a majority shareholding, like Thyssenkrupp did with Nucera. The consequence in this purely theoretical consideration: Capital inflow of over 2 billion USD, with which, on the one hand, the price for buying Hydrogenics is covered (flows back in); in addition, an extraordinary profit beckons; and thirdly, Accelera via the stock exchange would receive new growth capital (for acquisitions?) – just as a thought experiment.

Hydrogen-powered engines

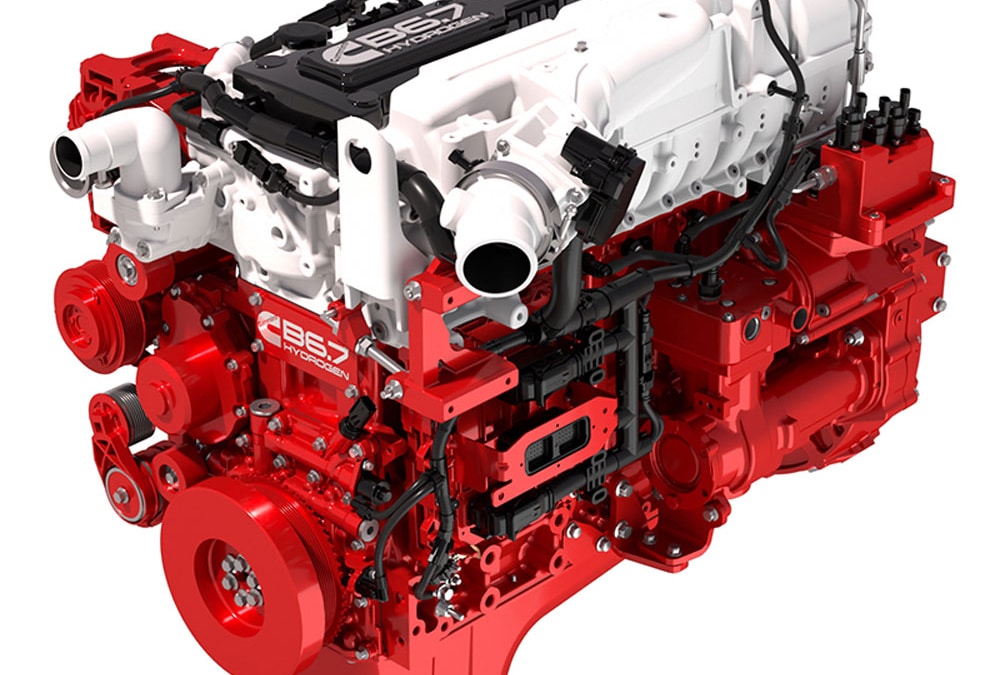

The automotive expert journal WardsAuto reports on how advanced Cummins is in its work to bring engines to market that run on hydrogen. There is to be a new version of the successful B6.7 diesel engine that with its powertrain burns hydrogen and can be used in heavy trucks. After all, there are already restrictions in place in California that prohibit already starting 2024 the operation of diesel trucks on, among other places, port grounds. Vehicles produced before 2010 will soon no longer be allowed on the roads of this state. A winning pass to all manufacturers of alternative drives – so employment of the fuel cell or direct injection of hydrogen as well as battery-electric systems.

With this, the new B6.7H 6.7-liter hydrogen engine (range of 483 km, or 300 mi) can quickly become a slam dunk if hydrogen and the corresponding infrastructure are available. So it is very suitable that the US government via the Inflation Reduction Act has provided 8 billion USD for the construction of six to ten H2 terminals distributed across the US – in addition to the many individual programs offered by states such as California.

Summary: Cummins Engine is working on a variety of platforms for the use of hydrogen in many applications such as heavy transport and rail but also for electrolysis, whether PEM or alkaline. The stock market will increasingly let this show in the company valuations. A real H2/FC blue chip is what Cummins has developed into.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.