The surprising takeover of the Canadian competitor Hydrogenics will also have a positive impact on Ballard Power’s stock market valuation: Both companies have been frontrunners in FC development for many years. Their activities overlap in rail vehicles and trucks. They are both absolutely tops: Hydrogenics with Alstom and Ballard with CRRC and Siemens. Ballard also has many other activities in the major markets of the future, such as the use of fuel cells in drones.

Depending on the order intake in the various areas and the standing of the customers, the stock exchange will increasingly increase the potential of the share and anticipate 2020/21, as in these years the clear transition from research and project work (prototypes) to operative markets is likely to take place. For strategic reasons, companies such as Bosch or Siemens should invest in Ballard. Bosch already cooperates with PowerCell and Nikola Motors, as well as with Weichai, which in turn is the largest single shareholder of Ballard and also of Kion/Still (material handling – forklift trucks etc.; 45 % share).

These overlaps also make capital links and cooperation in different markets, where synergies arise, useful. So far, Chinese companies (Weichai, Broad Ocean) hold about 30 percent of Ballard. Another major shareholder from Europe would be perfect not to leave the field unilaterally to the Chinese. Ballard has already positioned itself very well in China together with Weichai via its own stack production (LCS) and serves the world market (stacks for buses, trucks, forklifts, etc.) from there, while Weichai concentrates on China – a perfect geographical division of labour. However, I rule out a full takeover by the Chinese. That is where the Canadian state would put the stop sign

Current developments – 92 FC buses ordered

Solaris recently announced to Ballard an order for twelve fuel cell buses to be used in Italy. Wrightbus from Ireland has received another order for fifteen FC buses from Aberdeen, Scotland, for which the Canadians are also supplying the stacks. In total there are now 92 vehicles in Ballard’s order book – a nice start, but an order of magnitude that is only the beginning of major orders. You can be curious.

The European H2Bus consortium is already talking about 1,000 FC buses, all of which will probably receive the FC stacks from Ballard. The price development is interesting: Whereas five years ago a hydrogen-powered bus cost more than 1 million Euro and three years ago about 650,000 Euro, today (according to Ballard) the price is 375,000 Euro and the hydrogen price is expected to be between 5 and 7 US $/kg. A few years ago, a bus needed more than 20 kg for 100 km, today it is less than 7 kg/100 km. And in the long run, “green” hydrogen will cost no more than $2 to $3 per kg in production. The scaling effects have an effect.

Second quarter in line with expectations

Sales were expected to decrease slightly to $23.7 million and a non-GAAP loss of $0.03 per share was expected. The backlog of orders, however, grew to over US-$ 211.6 million. And the cash balance did not fall as I expected due to the investments in China but remains very high at $163.7 million at the end of the second quarter. According to Ballard CEO Randy MacEwen, the right growth of the company will come in 2020 – we can be curious.

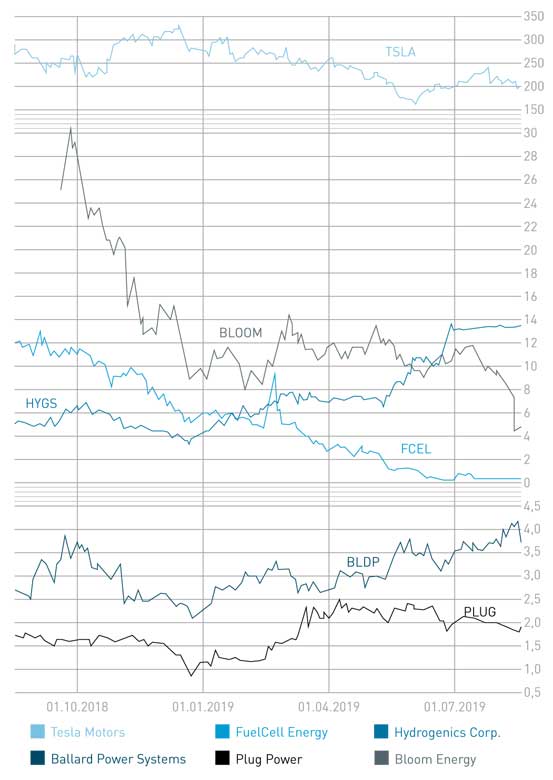

Conclusion: Ballard is and remains the key investment if you want to invest in the fuel cell on the stock exchange.

“We see a significant pipeline of projects that will feed into the 2019 backlog.”

Randy MacEwen, Ballard

Risk warning

Every investor must always be aware of his own risk assessment when investing in shares and also consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid-caps, i.e. they are not standard stocks and their volatility is also much higher. This report is not a buy recommendation – without obligation. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on a medium- and long-term valuation and not on a short-term profit. The author may be in possession of the shares presented here.

Author: Sven Jösting, written mid of August 2019

Sven, There is also an outstanding order of 2,000 modules to Weichai.