In the research project H2-Quartiere, the consultancy Steinbeis-Innovationszentrum Energieplus (here abbreviated SIZ E+) is investigating until 2024 how decentralized hydrogen production near to consumers through electrolysis (ELY) can be implemented. On behalf of the German ministry for economy and climate protection, six model districts equipped with ELY systems in urban and suburban areas of Baden-Württemberg will be analyzed and checked to see if there are technical-economic hurdles. The results will be presented in a market analysis for electrolyzers.

This study is based on 23 interviews with operators and manufacturers, with the analysis of the manufacturer market limited to companies that have a branch in Germany. For manufacturers without a branch in Germany, the rapid availability of service personnel in case of repairs or maintenance would be called into question. The results of this market analysis provide an insight into the current situation with regard to investment costs (CapEx), efficiencies and stack temperatures as well as challenges for operators in the distribution of green hydrogen.

Advertisements

Consideration of the operator side

In Germany, there are currently 13 publicly known electrolysis plants with a power consumption of more than 1 MW in operation (status in 2022, see Fig. 1). Together, these plants have an ELY capacity of around 70 MW. Out of seven interviewed operators of large ELY plants, two complained about the lack of standardization in the stack market. When replacing a stack, it would be advantageous to not be reliant on the same manufacturer that produced the first, it was said. One operator also expressed concern regarding non-European producers when it comes to rapid availability of service technicians in the event of a malfunction.

With regard to the politically envisaged scale-up, five out of seven operators noted that there are not enough customers or demand for green hydrogen to make further investments worthwhile. This is also demonstrated in the ways that green hydrogen has been utilized up to now. So far, six out of 13 large-scale electrolysis plants have fed their hydrogen into the natural gas grid. Only six supply hydrogen to the industrial and one exclusively to the mobility sector. For the benefit of the national economy and the environment, green hydrogen should be used primarily in industrial processes that are otherwise difficult to decarbonize [Agora Energiewende, 2021].

The experience of one plant operator was marked by various challenges. The construction process was delayed in particular due to delivery problems and poor performance by individual construction companies. The putting into operation and the approval process were made disproportionately difficult by additional safety requirements imposed by the responsible regional council. The operation after completion was burdened by sharply rising, volatile electricity prices. Despite these difficulties, the operator is planning to erect another, even larger, ELY plant. The company believes that the long-term ecological and economic potential of green hydrogen will prevail over the medium-term disadvantages.

Consideration of the manufacturer side

The investment costs (CapEx) of hydrogen-producing electrolyzers, regardless of process type, is about 1,000 €/kWel for a large plant. Comparison, however, is sometimes difficult, as not all producers offer the same scope with regard to supportive and auxiliary equipment (balance of power, BoP). The players surveyed are planning expansion with increasingly automated production lines, which could significantly reduce CapEx. For PEM electrolyzers, the share of BoP in the cost lay at 55 percent in 2020 [IRENA, 2020]. Since then, the market volume has increased. However, it can be assumed that here too considerable cost reductions will follow effective scaling.

Figure 2 shows the energy conversion efficiency (LHV to AC = lower H2 heating value to alternating current) of the total of 17 electrolyzers from nine different manufacturers, anonymized and sorted according to electrolysis process. These are alkaline electrolyzers (AEL) in addition to proton-exchange membrane (PEM) and anion-exchange membrane (AEM) electrolyzers. Only makes from manufacturers who are based in Germany and already have customer references are considered. Solid oxide electrolyzers (SOEL), because of the heat demanded by the process to achieve the high operating temperature, are not considered here.

Shown for each electrolysis process are the minimum, mean and maximum values from the manufacturer’s data. Regardless of process type, they vary little between the examined products, with AEL showing slightly higher values. However, the comparability of the manufacturers’ data is a question. Currently, there are no norms or policies to define a standard that indicates under which comparable conditions the efficiency should be determined.

It is striking that some manufacturers state the same system efficiency for makes of different sizes. This indicates that the power consumption of the BoP is only roughly accounted for. In the case of some data, it is unclear whether the specification of the efficiency is a snapshot of the “beginning of life” or an average over the whole lifetime. Furthermore, there is often no information about the load condition at which the efficiency was measured.

Through waste heat recovery, a significant increase in total system efficiency can be achieved. An important factor here is the temperature level of the waste heat source. Figure 3 shows the specifications of nine manufacturers with regard to the stack temperature during operation under nominal load. The stack temperature is the temperature of the cooling medium midway between the inlet and outlet from the stack.

The stack cooling is usually divided into two circuits via a heat exchanger: a primary circuit for direct stack cooling and a secondary glycol circuit for heat dissipation to the environment, for example via package crossflow cooling towers.

Regardless of process type, the difference between the stack entry and exit temperature is usually not significantly more than 10 Kelvin, as higher spans can lead to higher degradation and inhomogeneous load conditions in the stack [TU Delft, 2019]. The primary cooling circuit, because of the special demands on the cooling medium imposed by direct contact with the cells, is usually separated from the glycol circuit via a heat exchanger. For proper hydraulic separation, another heat exchanger may be required in the secondary glycol circuit for waste heat extraction. If a temperature difference of, for example, 10 K is the target, then the return flow temperature from the waste heat utilizer must be between 15 and 20 K below the stack temperatures in Figure 3.

In light of this, all current products, in combination with a peak demand power station via a local heating network, are suitable for supplying an existing or new building area with heating energy. The temperature of most AELs, at an average of 76 °C, is theoretically high enough to enable the supply of hot tap water where appropriate. In practice, however, there are hurdles that can make the use of waste heat difficult. In containerized systems, compact heat exchangers with small transfer surfaces and high temperature differentials are often used, which requires extremely low entry temperatures on the part of the cooling medium. When using a heat pump, this entry temperature is decisive for the evaporating temperature of the refrigerant. To ensure a high efficiency, or rather coefficient of performance, of the heat pump, larger heat exchangers and higher entry temperatures are advantageous.

The principle of waste heat utilization for heat supply had already been implemented by SIZ E+ in the climate-neutral city quarter (Klimaquartier) established in Esslingen am Neckar in the state of Baden-Württemberg (see H2-international May 2021). The project is based on the idea of a climate-neutral quarter with the lowest possible carbon footprint. The heart of the energy supply is an AEL plant with an ELY capacity of 1 MW, which receives surplus electricity from local photovoltaic systems as well as from other regions. The ELY waste heat at the same time serves as an energy source for a heat pump. The project follows the innovative approach of power-to-gas-and-heat, in which hydrogen is to be produced close to the consumer on a local level at sensible nodes.

In the new project H2-Quartiere, the potential implementation of this approach in six other model neighborhoods is being explored. Through the use of waste heat in the conversion process and through the short transport routes to the end users, this system approach is potentially extremely efficient and offers highly synergistic effects to the much needed clean heating and energy transition. According to the 2021 study by the German real estate association ZIA, around 20 percent of the heating demand in the buildings sector could be covered by ELY in year 2045 if half of the German hydrogen demand is produced by local ELY plants within Germany [ZIA, 2021].

Tiktak, W. J. (2019), “Heat Management of PEM Electrolysis,” TU Delft Master Thesis, p. 19, http://resolver.tudelft.nl/uuid:c046820a-72bc-4f05-b72d-e60a3ecb8c89

Flis, G. et al. (2021), “12 Insights on Hydrogen,” Agora Energiewende, p. 16, https://static.agora-energiewende.de/fileadmin/Projekte/2021/2021_11_H2_Insights/A-EW_245_H2_Insights_WEB.pdf

Fisch, M. N., Lennerts, K. et. al (2021), “Verantwortung übernehmen. Der Gebäudebereich auf dem Weg zur Klimaneutralität,” ZIA Zentraler Immobilien Ausschuss, pp. 144-145, https://zia-deutschland.de/wp-content/uploads/2021/12/Verantwortung-uebernehmen-Gutachten.pdf

IRENA (2020), “Green Hydrogen Cost Reduction: Scaling up Electrolysers to Meet the 1.5⁰C Climate Goal,” International Renewable Energy Agency, Abu Dhabi, p. 52, https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2020/Dec/IRENA_Green_hydrogen_cost_2020.pdf?rev=4ce868aa69b54674a789f990e85a3f00

Authors: Prof. Dr. M. Norbert Fisch Dr. Christian Kley Benjamin Trippe benjamin.trippe@siz-energieplus.de Simon Marx All from Steinbeis-Innovationszentrum Energieplus, Braunschweig

Image: Current commercially operated electrolysis plants in Germany

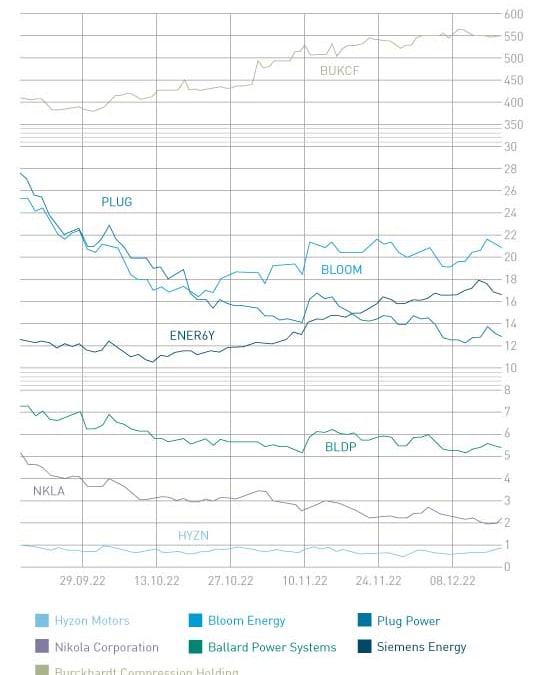

The turnaround we’ve been forecasting for some time is in sight. Year 2024, according to the predictions of board chairman Christian Bruch, will bring profit. The share price has turned around noticeably and rose nearly 50 percent compared with the lowest price. The numbers: The turnover of 29 billion EUR lay in the realm of expectations (minus 2.5 percent is due to extraordinary developments – to Ukraine alone is attributed a loss of 200 million EUR). There was a loss in the amount of 647 million EUR, which is a consequence of integrating the nearly 1 billion EUR reported loss from Siemens Gamesa.

The order volume is excellent: This rose in the fourth quarter, based on 2022/09/30 data, to an equivalent of 97.4 billion EUR – a good basis for the future of the corporation. Growth of three to seven percent is now expected and depends on Siemens Gamesa being able to be fully integrated in the next 12 to 24 months and ultimately also generate a positive profit contribution.

Advertisements

Stock market valuation was a joke

Siemens Energy was still valuated a few weeks ago at just 8 billion EUR, but the current value of around 12 billion EUR does not correspond to the potential of this big business. For the weak stock market price, the planned acquisition of the remaining shares in the wind subsidiary Siemens Gamesa was to blame, as there were audits by the Spanish regulatory authority (CMMV) that dragged the integration, or full takeover, out even longer. And clear is also: 2,900 jobs (10% of total workforce) will be cut and the company Gamesa will become part of Siemens Energy.

The positioning of Siemens Energy in important future markets such as hydrogen (order boom!), however, will sooner or later need to lead to a revaluation of the corporation – in accordance with the sustainable profit and increasing sales. Based on the current ridiculous valuation, Siemens Energy could even be a candidate for takeover. Nothing is impossible.

Those who bet on the turnaround will build up new positions or cheapen existing ones. This will not be a quick fix but should be an investment over a period of at least one to three years. There will still be many a quarter of losses, which is the fault of the costs of reorganization and the integration of Siemens Gamesa. On the other hand, there are many exciting technological developments such as rotor blades for wind turbines that can now be recycled, which has been a major problem so far.

Since a few days ago, you can see a turnaround in the stock. The stock market anticipates future developments, so little by little there will be better prices again. Since big investors like BlackRock have the area Siemens Energy is in in focus, a lot of new capital will flow in from here. In addition, Siemens Energy is back in the DAX. Stay tuned. My price target within the next 12 to 18 months: 30 euros plus.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: written by Sven Jösting December 12th, 2022

We’re seeing a steep decline in earnings at Weichai Power: 2.387 billion CNY gain (minus 63.3 percent compared with the previous year) with a 35.9 percent turnover decrease to 86.74 billion CNY. The subsidiary Kion (45% stake) even saw its share price fall on the stock market from over 120 to 20 EUR (recently strongly increased again) due to a profit slump in the course of the year: 210.6 million EUR gain after the 691.1 million EUR in the prior-year period of the first nine months, although turnover in the reported period was able to be upped from 8.24 to 8.4 billion EUR. Supply chain problems as well as cost increases (for raw materials, etc.) were cited as the basis.

Weichai’s valuation – compared to the 30 billion USD of Cummins Engine – is quite low: just 10 billion USD for the market leader in diesel engines in China. In the third quarter, it suffered a slump in diesel engine deliveries to 136,000 units, which corresponds to a 32 percent decline. Shareholders are viewing all this critically, but there are still psychological influences that can’t be accounted for in this type of assessment.

Advertisements

There’s no doubting the fact, however, that China is committing increasingly more to hydrogen and fuel cells, and Weichai will clearly be among the beneficiaries, as they are perfectly – also see Ballard – positioned. For us, a key investment in the hydrogen sector of China. The share has moved noticeably upwards again in recent weeks and should be able to reach quite different, and indeed higher, rates in the coming years, when the fuel cell strategy outlined in the national provisions gains momentum in implementation.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: written by Sven Jösting December 12th, 2022

It’s kicking off in the USA: The Inflation Reduction Act with its billions in funding (369 billion USD), among other things for the ramp-up of the hydrogen economy, is giving hope. I was able to witness this myself live via video stream at the 2nd Hydrogen Americas Summit. In Washington, many board members of well-known companies showed their histories with hydrogen and reported their plans. Hydrogen has always had a place, but the time is now here to massively expand its scope in order to solve environmental and climate issues and to see hydrogen as a game changer for the world.

Energy security too was stressed. The next ten years in hydrogen development will change the world, during which the US plans to produce an initial 10 million metric tons per year. It is fundamentally different today than it was in the decades before. The mix of measures for the ramp-up can be listed as follows:

Advertisements

– Incentives (tax breaks, cash grants)

– Policy framework (regulations, standards)

– Demand conditions (markets)

– Climate influence (climate change questions)

– Energy security (security of supply)

– Inflation Reduction Act as an initial spark

There’s need to become H2-ready. This entails conversion of existing infrastructure (gas pipelines, etc.) for hydrogen. There’s already an infrastructure for ammonia, so green hydrogen will see its first big market here if ammonia is used as a medium for transporting hydrogen alongside the use in fertilizer production.

The issue of hydrogen must be approached locally as well as globally at the same time, it was said. For this, cooperation between old industries and new players is necessary, and even a prerequisite and condition for a successful ramp-up of the hydrogen economy. The other side must also be taken into account, however, which is based on jealous competition, market prevention and protection of vested interests, since not all players find the development good.

But healthy competition is also needed. Here, government representatives from Canada and the US came in, and according to their statements, competition in the implementation of a hydrogen strategy will occur with true sportsmanship. Demand must be created for hydrogen. One of the first markets will be transportation (here: commercial vehicles, ships and trains) as the “driving force & source.”

A statement from Christian Bruch, board chairman of Siemens Energy, regarding the Act described it best: “This will bring about investments from many companies in the US. One can certainly debate whether America is funding too much and fueling subsidy competition, but the need for renewable energies is far too great everywhere. What makes America different from Europe: the USA is open to technology. There isn’t talk about green or blue hydrogen, but about hydrogen. The subsidy eligibility conditions are simple; everyone can understand them. There’s a wave coming that has the chance to reindustrialize the USA.”

There are 18 sectors in which hydrogen is needed. It will start off with “early mover markets,” to which heavy transport belongs (heavy-duty trucking industry). But other markets will also emerge and grow, like communication towers, as there are over 600,000 in India powered by diesel engines and 10,000 police radio towers in the USA that in the future will be powered by hydrogen via fuel cells. In the case of forklift trucks, we can already see that more and more are running on hydrogen instead of diesel or battery-electric.

Many market participants are suddenly all seeing their future in this market at the same time. Here, comparisons can be made to the beginning of the Internet, of the WWW, which changed the whole world as a new disruptive system. Whether financiers (banks, VCs) or technology suppliers, consulting firms, clients or governments – they now all want to enter the hydrogen age.

Also heard were comparisons to the beginnings of the solar industry, where 30 years ago, one kWh cost 2.50 US dollars, and today, only 0.025 cents. With batteries, it took 15 years for the energy density and price to initiate a new market. The same will happen with green hydrogen, for which the majority of analysts foresee a price of 1 USD per kg for year 2040, and expect 1 to 2 USD per kg already by year 2030.

Hydrogen will be obtained from many sources, including biogas and waste recovery. With this, it should also be “grid-friendly,” meaning able to be transported and used in the existing infrastructure (for example blended in the natural gas grid). The optimization of all components as well as their integration in particular will take on importance.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: written by Sven Jösting December 12th, 2022

Those who weren’t familiar with Refire before can now think of the fuel cell company every time they hear the name Clean Logistics, because the startup from Niedersachsen has a supply contract for fuel cell systems from the company. So it’s not surprising that Audrey Ma, Refire Group Vice President International Markets, had been invited to be a guest of honor at the presentation ceremony for Clean Logistics’ truck Fyuriant truck launch this past summer in Stade (see H2-international Oct. 2022). H2-international had the opportunity to speak with Ms. Ma during IAA Transportation 2022 in Hannover.

H2-international: Ms. Ma, how long has Refire been around and how long have you been with the company?

Advertisements

Ma: Yesterday was actually the seven-year anniversary of the Refire Group. It started out as a very small team. The founders were three engineers who worked in the area of fuel cell technology. I joined the company at the beginning of 2017 and within these few years, we’ve grown to a team of nearly 700.

What was your goal at the time?

Our common goal was to further develop fuel cell technology for commercialization, which is now all around us at this trade fair. I believe we’ve contributed to making fuel cell technology market ready.

Could you give us examples of how?

In 2017, we put our first FC vehicle fleet – 500 7.5-tonne fuel cell delivery trucks – on the road in Shanghai. We engineered and manufactured the fuel cell systems and worked on further development of the vehicle prototype, including FC system integration. Our partner at the time, Dongfeng, which is a major Chinese OEM, then built the 500 trucks. This was a really challenging undertaking, and we learned a lot from it – from hydrogen production to the question of who would do vehicle maintenance work. We managed to find operators that would use these vehicles and market them to end-user companies. When we mobilized drivers, we were also the ones who then organized the after-sales service of those vehicles, not the OEMs or the operators. After that, we redoubled our efforts and, among other things, we installed an H2 station of our own with partners so that our drivers would have a place to refuel.

In other words, a completely new approach to bringing such technology into the hands of customers.

Yes, we had to take a different path. We had to find ways to make it viable because a traditional approach wouldn’t have worked here.

Why are you here today?

We brought a fuel cell system with us today that came straight off the production line. This is not a prototype. We will have covered over a million kilometers with this system by the end of the year. It has a power output of 117 kW and has already been integrated into several hundred heavy-duty vehicles. We are working together with a variety of partner companies – domestically and internationally, including in Germany, to integrate these systems into vehicle powertrains.

So you’re a classic system integrator.

Yes, we integrate fuel cell technology in various applications. The Refire Group has three subsidiaries that develop FC technologies and manufacture products. One of the business units, Unilia, produces FC stacks. Another, Pando, makes FC power electronics products, and Refire Technology builds complete FC systems. These three subsidiaries operate independently but under a common umbrella.

So you produce your own fuel cell stack but also use stacks from other producers for your systems, like Ballard for example?

That is correct. In the production of complete FC systems, our own stacks or those from other manufacturers may be used. For example, in one project Toyota is our stack partner. Similarly, there are also German, Canadian and Chinese stack suppliers that we have worked with.

I see. What applications do you address with Refire Technology?

We focus on a variety of applications for commercial vehicles and stationary power. We don’t just supply the fuel cell systems and core components, but also offer application engineering services. Sometimes we’ll also do turnkey solutions in order to help customers decarbonize specific and unique end use case applications.

Is that what you do for Clean Logistics?

Clean Logistics has a very capable engineering team which already has experience from past work in the conversion of diesel powertrains to battery-electric, and they’re now adding fuel cell solutions to their product lineup. The complete engineering solution that we typically provide OEMs is to integrate a fuel cell powertrain based on their own existing chassis. We look at which fuel cell system is optimal for a given application, and then we assemble the various vehicle components in order to return a fully finished fuel cell vehicle prototype to the OEM.

How many systems have you already delivered?

We have shipped in total about 4,500 fuel cell systems for commercial vehicle integration. Vehicles powered by Refire FC systems have now converted at least 3,500 tonnes of hydrogen into electricity for zero curbside emission driving. Altogether, the fuel cell commercial vehicle fleets have clocked more than 125 million kilometers, a mileage that rises about 1 million kilometers every week. As I mentioned earlier, our aim has always been to commercialize fuel cell technology, and so bringing products to market and into the hands of actual drivers is very important. We work collaboratively to enable OEMs to homologate their prototypes so that at-scale vehicle production can be achieved when fleet operators place their orders.

You’re based in Shanghai, and are also active in Germany and North America. Where is your global focus?

That’s right – Refire’s corporate headquarters is in Shanghai. We currently have two engineering centers – one in Shanghai, and another in Vancouver. A third engineering center is in the works in Germany which will service our European customers.

According to concerted opinion, hydrogen is now considered the new universal energy carrier that is set to take the place of fossil energy sources in gas heating systems, cogeneration plants, cars, steel works and the chemicals industry. This is also recognized by Scientists for Future. In a recently published policy paper they describe hydrogen’s essential place in the energy transition yet also point out that its use is inadvisable in many areas on technical, economic and environmental grounds. The key sections of this paper are set out here:

In principle, hydrogen can be transported in the same way as natural gas via pipelines or tanker vessels and stored in tanks or caverns. This suggests that green hydrogen, in other words decarbonized hydrogen that is produced electrolytically with renewable power, could act as a replacement in all situations where we currently use fossil-based raw materials such as crude oil and – above all – natural gas. This belief is deceptive since for many purposes the deployment of green hydrogen is much too expensive and is an inefficient use of energy. Ultimately we will only use green hydrogen in cases where natural gas and crude oil cannot be replaced by the direct application of electricity or where hydrogen is the base material, for instance in the chemicals industry or in the carbon-free manufacturing of steel.

Advertisements

A calculated optimism is clearly evident in some studies by natural gas network operators: The German gas and water industries association DVGW, whose membership includes over 2,000 utility companies, does not work on the basis that there will be a shortage of hydrogen. A study published by the DVGW calculates that high demand will be accompanied by an equally high degree of availability of more or less sustainable hydrogen (Gatzen & Reger, 2022). Underpinning this is the unsupported assumption that there will be an import rate of 90 percent, in other words the same level as today’s oil and gas imports.

“Just supplanting one fuel with another will not suffice for the energy transition. The energy transition inevitably requires a shift away from traditional technologies and habits.”

These optimistic assumptions on the availability primarily of imports are at the center of the argument that hydrogen would be available even for heat provision: “In contrast to the frequent assumption, hydrogen does not have to remain a scarce good. The demand for hydrogen can be more than covered from 2030 onward. The quantity exceeds all current demand forecasts many times over” (DVGW, 2022, p. 5). This strikingly optimistic supposition can be confirmed neither technically nor scientifically.

At least 10 years will pass before larger quantities can be imported. And what often goes unsaid in relation to desired hydrogen imports is that the transportation is so expensive that imported hydrogen will cost many times more than today’s natural gas or crude oil. On this point it makes no difference whether the hydrogen is transported in a compressed, liquefied or chemically bonded form.

The use of hydrogen is only wise if it is produced with renewable electricity (green hydrogen). In future this will also be the cheapest production method. Hydrogen manufactured from natural gas (gray or blue hydrogen) and hydrogen from methane pyrolysis (turquoise) are not carbon neutral due to the use of natural gas and the upstream emissions from methane; and excessive risks and long-term consequences are associated with the use of nuclear energy for electrolysis as an ecofriendly method of producing hydrogen (pink).

Analysis of individual application areas

The need to use hydrogen is already on the horizon in certain sectors. This affects, for example, iron and steel production as well as the chemical raw materials industry and hydrogen as an energy storage medium. At present, refineries require hydrogen for several processes, including the cracking of crude oil when manufacturing fossil fuels. This area of current hydrogen demand will disappear in the future. In other applications, hydrogen competes with other good solutions:

In vehicles, e.g., automobiles, electric propulsion is the most efficient and most practical solution. It is for this reason that manufacturers have practically given up on hydrogen propulsion for the future (Clausen, 2022). The situation for delivery vehicles, city buses and railroads can be said to be similar. Even when it comes to long-distance trucks, the Fraunhofer Institute for Systems and Innovation Research points out that, should the first hydrogen trucks be available in 2027, the second generation of battery-electric trucks will already be on the road (Plötz, 2022). The window of opportunity for successfully launching fuel cell trucks onto the market would therefore be essentially closed and all that would be left for hydrogen trucks would be a small niche, namely the transportation of heavy loads to very remote locations (Plötz, 2022).

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.