The Swiss energy corporation Axpo has identified hydrogen as a field for strategic growth. The H2 production facility at Kraftwerk Reichenau – the power plant on Reichenau Island – is one of several set by run-of-the-river hydropower plants that Axpo has planned for the coming years. Because Switzerland is striving for climate neutrality by 2050. Green hydrogen is playing a central role in this – particularly to decarbonize the heavy transport sector.

Advertisements

Axpo is the largest producer of green electricity in Switzerland. By 2030, the energy corporation wants to have installed in the domestic market alone 3 GW of wind power plants and 10 GW of solar. The energy supplier, however, also wants a part in shaping the future of green hydrogen in Switzerland and Europe. Because the Alpine republic currently has a total H2 consumption of 430 GWh, or 130,000 tonnes. In perspective: This corresponds to 0.2 percent of EU demand. And 85 percent of this consumption is alone attributable to the Swiss petroleum refinery Raffinerie Cressier.

First H2 production end of 2023 in Graubünden

Visible results can already be seen from the new strategic field. Axpo and Rhiienergie have installed at hydropower plant Wasserkraftwerk Reichenau in Domat/Ems an H2 production plant with a capacity of 2.5 MW. The plant is to go into operation at the end of 2023. The two companies have together invested the equivalent of over 8.35 million euros. The production facility will be directly connected to Wasserkraftwerk Reichenau, in which Axpo holds a majority interest, situated in the canton Graubünden.

At this site, up to 350 metric tons of green hydrogen are to be produced annually using hydropower. This is analogous to about 1.3 million liters of diesel. The green hydrogen will be delivered from the production plant directly to refueling stations. Alternatively, the green hydrogen could additionally help make energy supply for industrial operations more eco-friendly.

So far, likewise to Germany, hydrogen has not been widely used as a fuel in Switzerland. A network of fueling stations is only slowly being established, although the first H2 trucks are already on the roads. H2 mobility remains a niche area for now. Nevertheless, the current 53,000 heavy vehicles in Switzerland offer great potential for the growth of a future hydrogen market in the coming years. A demand of around 5 t H2 per truck per year from this market is quite realistic. If so, 30 percent of the vehicles would then require 80,000 t H2. At 5,000 operating hours per year, this would necessitate an electrolysis capacity of 1,000 MW.

Environmental and heritage protection prevent expansion

Not all of the innovative projects will see a successful implementation, as the resistance from some persons with an interest in nature and heritage protection is in some places simply too strong. One example is wind energy: The time for the planning and design phase of projects is enormously long; time and again, they do not advance. The result: In the whole of Switzerland, just 41 wind power plants are running. Axpo operates only one of these, through its subsidiary CKW.

But the protest is not limited to wind power alone: Earlier this year, an H2 project on the Swiss-German border was halted due to objections made by local residents (see H2-international Feb. 2023). “The hydrogen production facility at Wasserkraftwerk Eglisau-Glattfelden has been tanked as a result,” confirmed Axpo CEO Christoph Brand. Three private individuals had lodged protests. They did not want one truck once per day driving through their residential neighborhood and picking up the hydrogen, Brand explained. In addition, however, a power generation structure erected outside of the developable land zone will have to be demolished and placed elsewhere, as the court did not grant it exception approval from the zoning. The H2 plant when finished was to likewise have a capacity of 2.5 MW and produce around 350 tonnes of green hydrogen annually. That is now history. The green gas must come from elsewhere – from Northern Europe, among other places.

Fig. 2: The H2 plant under construction

Luka Cuderman, who as energy manager at Axpo is working on the strategic direction of the future H2 business, summarized the general requirements for an H2 production site once more. So the power plant itself needs sufficient space and connection capacity. Outside of the buildable land zone, according to his statements, certain constraints must furthermore be met in order to conform to zoning restrictions and be allowed there. Equally important are proximity to end consumers as well as a good connection to transport routes. “A secondary application such as utilization of incidental waste heat is a further plus,” stressed Cuderman.

The electricity price is the determining factor for H2 costs here. It accounts for more than half of the total cost. The investment costs, the capex, of the plant are in turn directly linked to the number of operating hours. An increase of this working time is only sensible under certain conditions, however, since operation at high electricity costs is uneconomical. “For the example of an electrolyzer with 2.5 MW, we assume 5,500 operating hours,” stated Cuderman. The cost of operating the plant, or opex, accordingly accounts for twelve percent of the H2 cost per kilogram. Grid costs do not incur for the operation if the H2 plant is directly connected to the power source. That is, however, not always the case.

Summary: The more hours an electrolyzer can work, the more weight the electricity costs take on. So close to full load, the cost for electricity constitutes 80 percent of costs.

2,000 t H2 per year from Aargau

Axpo wants to advance the topic of hydrogen in its homeland in another way: At the industrial park Wildischachen in the canton Aargau in Northern Switzerland, a still larger production facility is to soon appear. It is designed to have up to 15 MW of installed capacity. Annually, 2,000 t of hydrogen is to be made available. The electricity required for production is coming entirely from the nearby run-of-the-river power plant Flusskraftwerk Wildegg-Brugg. With direct connection to the hydropower plant owned by Axpo, climate-neutral production of hydrogen will be ensured.

The H2 produced will then be delivered partly to the nearby refueling station of company Voegtlin-Meyer via a pipeline and partly to other refueling stations in the region. The green hydrogen is to be made available to private users, on the one hand, as well as used in H2 buses for public transport commissioned by the company PostAuto. With the produced H2 quantities, around 300 trucks, PostAuto vehicles or buses can be run per year.

The utilities provider IBB is designing the pipeline that will lead from the H2 production plant to the refueling station in Wildischachen. The waste heat resulting from the electrolysis process is to be utilized in the heat network of neighboring industrial operations. The location of the plant is therefore ideally selected, as it is in the direct vicinity of the Axpo hydropower plant in Wildegg-Brugg and of the refueling station of Voegtlin-Meyer. The construction and start-up of the H2 plant is planned to occur in the course of 2024. Which is when the fleet of PostAuto is to be supplied with green hydrogen. So in Switzerland as well, the niche for green fuel is starting to grow.

Hesitant politicians put the brakes on the expected upswing

Activities in the Norwegian hydrogen industry have doubled in the last two years. Great progress has also been made in cooperation with Germany to be able to export hydrogen on a large scale from 2030. However, in order to move from project planning to investment decisions, risk relief in the form of contracts for difference is required.

In October 2021, the minority government led by the Labour Party and the Center Party announced in its government platform that it will contribute to building up a coherent hydrogen value chain where production, distribution and use is developed in parallel. It also announced that it will set a target for yearly production of renewable and low-carbon hydrogen by 2030 and to consider setting up a state-owned hydrogen company.

Advertisements

Hydrogen is a vital part of the government’s roadmap for an industrial revival on the Norwegian mainland. Norwegian petroleum and energy minister Terje Aasland has on several occasions stated that the government plans to have enough domestically produced hydrogen to cover own demands by 2030. However, the government is yet to reveal how much demand it expects or how it plans to achieve this.

Although industry is awaiting a clear path and ambition from the politicians, much has already been set in motion. The 2020 Norwegian Hydrogen Strategy emphasizes that Norwegian industry is well positioned to take a leading role in the hydrogen economy, concentrating efforts on areas of particular potential for industry growth and value creation, such as clean hydrogen production and offtake in the maritime sector and heavy industries.

The strategy was complemented by a Hydrogen Roadmap in 2021, which provides an ambition to establish five hydrogen hubs for maritime transport, one or two large industrial projects with production facilities for hydrogen and five to ten pilot projects for the development of cost-effective hydrogen solutions and technologies by 2025. The Norwegian state agency Enova in December 2021 granted support to three large industrial projects – led by Yara International, Tizir Titanium & Iron and Horisont Energi – and in June 2022 followed up with further support to five hydrogen hubs along the Norwegian coast, as well as 7 hydrogen and ammonia vessels. Further, the government has provided funding for two research centers of expertise on hydrogen and ammonia.

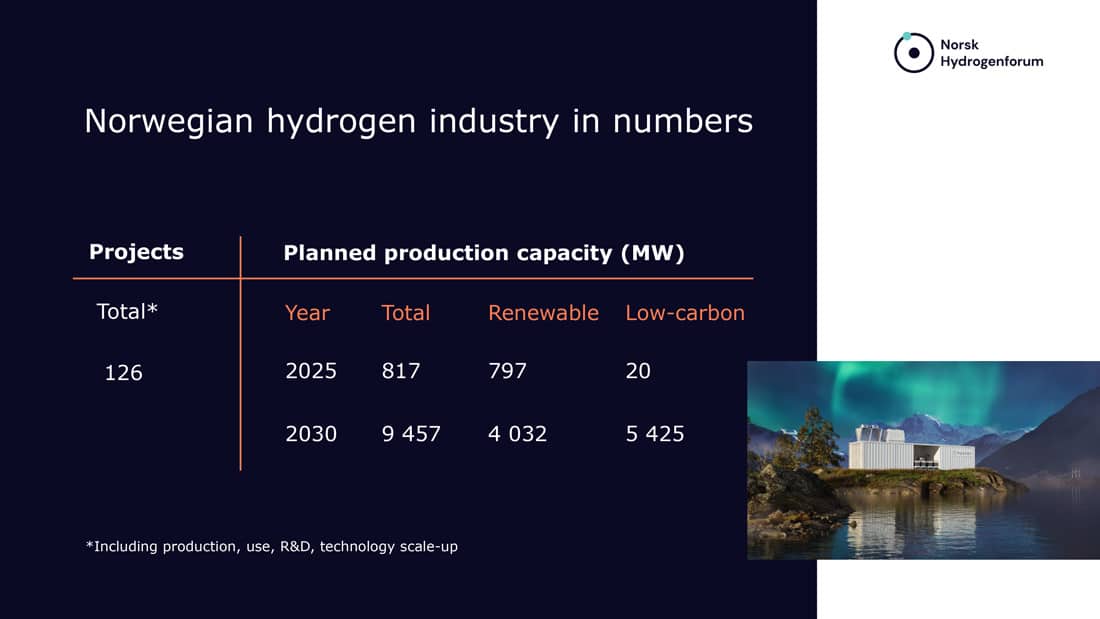

From 50 to 126 projects in two years

We at Norwegian Hydrogen Forum recently conducted a screening of the Norwegian Hydrogen Landscape,[1] and what we found was that the number of projects and activities had more than doubled since our last screening – from approximately 50 projects in 2021 to 126 in April 2023. We found 51 plans to produce hydrogen or hydrogen derivatives, totalling a projected production capacity of almost 9.5 GW by 2030. Although 47 of these projects are renewable hydrogen projects, almost 60 percent of the projected production capacity is expected to be low-carbon in 2030 (see image). Whereas most of the renewable hydrogen projects are planned for domestic consumption, three of the four low-carbon hydrogen projects are export-oriented.

With a capture rate of around 95 percent, using Norway’s vast natural gas resources and storing the captured CO2 under the seabed to produce hydrogen with extremely low emissions is seen as the smartest way forward by politicians and industry alike. In this way, the hydrogen market can be rapidly boosted, the necessary infrastructure built, and the way paved for the huge volumes of renewable hydrogen. Large quantities of green hydrogen can be produced from the late 2030s, when offshore wind power production on the Norwegian continental shelf gains momentum.

With a capture rate of around 95 %, utilizing Norway’s vast natural gas resources and storing the captured CO2 below the seabed to produce hydrogen with extremely low emissions is generally seen by politicians and industry alike. In this way, the hydrogen market can ramp-up quickly, to build the necessary infrastructure and thereby to pave the way for the massive amounts of renewable hydrogen. Large quantities of green hydrogen can be produced from the late 2030s and onwards as offshore wind energy production picks up speed on the Norwegian Continental Shelf.

To enable this, the Norwegian government supports the establishment of a full-scale value chain for carbon capture, transport and storage in the North Sea. The Longship project is ongoing, in which 400.000 tonnes of CO2 from Heidelberg Cement’s plant at Brevik shall be stored permanently below the seabed by the Northern Lights Joint Venture. The Norwegian government has also conducted several licensing rounds for further CO2 storage sites, and the offshore industry currently has plans to develop up to 50 million tonnes of yearly CO2 storage capacity by 2030.

Among the projects are several hydrogen technology manufacturing facilities, of which the most well-known is Nel Hydrogen’s recent opening of the world’s largest automated factory at Herøya. Both Hystar and HydrogenPro also have bold ambitions for electrolyzer manufacturing, and Norway is particularly well-positioned to contribute to a large share of the 100 GW electrolyzer manufacturing capacity needed in the EU to reach its 10 million tons of renewable energy production target.

Further, there are currently several plans to scale fuel cell manufacturing in Norway. For example, TECO 2030 is building up Europe’s first giga production facility of hydrogen PEM fuel cell stacks and modules in Narvik and targets 1,6 GW output capacity in 2030. On May 15th, they produced their first stack. These and other companies could sharply increase and multiply their manufacturing capacities in Norway.

Local companies shoulder development of H2 economy

The actors involved in building up the Norwegian hydrogen industry come partly from the country’s strong historic research and industrial community on hydrogen and hydrogen technology. Norway produced its first ammonia from hydropower and water at Hydro’s Rjukan site already in 1929. But also from the strong renewable industry, the maritime industry, and the offshore oil and gas industry. In addition to significant competence in the fields of electrolyzers, fuel cells, storage tanks and hydrogen refuelling stations, Norway is at the forefront when it comes to developing new solutions in areas such as carbon capture, compressors, bunkering solutions for maritime application, hydrogen and ammonia ships and innovative concepts for offshore hydrogen production. The country’s substantial sub-suppliers in the oil and gas industry can further utilize its competence to develop renewable and low-carbon equipment and appliances for the hydrogen economy.

Private-public collaboration

Although there is political agreement that the CO2-price shall increase from 952 NOK in 2023 to 2.000 NOK by 2030, there is still a challenge that fossil fuels are cheaper than hydrogen-based fuels. To go from project planning to final investment decision, there is a need for a public-private partnership in which risk relief is given until hydrogen reaches price parity with fossil fuels. The favoured measure among Norwegian Hydrogen Forum’s members is a Contracts-for-Difference (CfD) scheme.

We have suggested to the government that a first auction should take place as soon as possible in 2024 to ensure predictability for the many companies that are now at a stage where they must take final investment decision or look for other projects. In last year’s approval of the state budget, the Norwegian Storting (parliament) requested the government to develop a plan for a CfD scheme in 2023. Petroleum and Energy Minister Terje Aasland has confirmed that the government will deliver this plan accordingly.

Great leap for German-Norwegian partnership

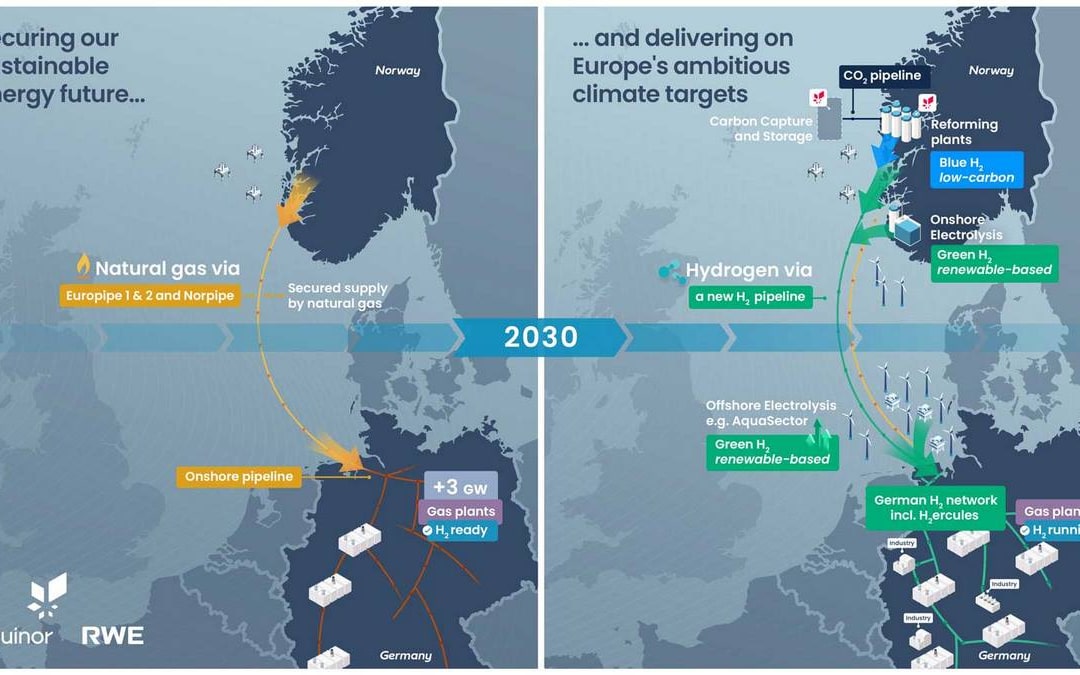

Whereas uncertainties remain when it comes to developing the domestic value chain for hydrogen, several giant steps have been taken to establish a value chain for large-scale hydrogen exports from Norway to Germany. In January 2022, Norwegian prime minister Jonas Gahr Støre issued a new era of bilateral energy and industry collaboration when he visited German chancellor Olaf Scholz in Berlin to set up a renewed energy and industrial partnership between the two countries. Since then, ministers from both countries have travelled back and forth in an impressive tempo, not least due to the Russian full-blown invasion of Ukraine a month after Støre’s visit.

Since Vice-Chancellor Robert Habeck visited Oslo in March last year, a feasibility study on large-scale exports by pipeline has been ongoing, and the result of that study is expected soon. If a decision is taken to go forth with the plans to build a pipeline, Norway could by the beginning of the 2030s export two to four million tonnes of hydrogen directly to Germany (see fig. 1). The pipeline will be built with dimensions that are 30 % larger than current low-carbon production plans and will have the capacity to include renewable hydrogen both from the Norwegian mainland and from offshore wind farms along the way.

The close political collaboration has been followed by a string of industrial collaboration projects. Firstly, we have a Memorandum of Understanding (MoU) with the German Hydrogen and Fuel Cell Association (DWV), with which we regularly meet in different settings, for example at stage at this year’s Hannover Messe to discuss the importance of the German-Norwegian partnership .

Secondly, we have a strategic cooperation agreement with Center Hydrogen.Bavaria (H2.B), which we visited with a delegation during a political roundtable meeting in January. Hopefully, this collaboration will contribute both to set up hydrogen exports even to the alps and to scale up the number of heavy-duty trucks with hydrogen as fuel on Norwegian roads soon. The five northern German states (HY-5) also have a formalized collaboration with the Norwegian support agency Innovation Norway.

Equinor and RWE agreed beginning of this year, to cooperate on building hydrogen-ready gas power plants, to jointly develop offshore wind farms that will enable production of renewable hydrogen, and to build low-carbon hydrogen production facilities in Norway with the intent to export by pipeline from Norway to Germany. VNG collaborates with Equinor on the H2GE Rostock project, but also has ongoing collaboration with Aker Horizons and Yara. The German utility EnBW is active in the Norwegian market within development of offshore wind and has advanced negotiations with Skipavika Green Ammonia. On the electrolyzer side, Nel Hydrogen will deliver components for two hydrogen facilities under development by HH2E. Norwegian hydrogen producers also have very good collaboration with German electrolyzer producers, such as Fest and H-Tec. It is probably not a surprise that when the world’s first ferry powered by liquid hydrogen, MF Hydra, came into operation earlier this year, it was Linde that delivered both the hydrogen and the bunkering solution.

These are just a few examples that show the vast opportunities for hydrogen in Norway. Collaboration with Germany will be paramount in realizing this potential, and I am certain that when we yet again screen the Norwegian hydrogen landscape in 2030, we will be seeing an industry in Norway that gives a vital contribution to European emission reductions and energy security.

Author: Ingebjørg Telnes Wilhelmsen, General Secretary, Norwegian Hydrogen Forum

Norwegian Hydrogen Forum (NHF) was founded in 1996 and is the national association for the hydrogen and ammonia industry in Norway. NHF works actively to disseminate key information on hydrogen and ammonia research and technology commercialisation, market trends and international policy making. Its core task is to promote its members’ interests towards public authorities and decision makers.

If hydrogen is expected to change the world, then the associated industries need to massively expand their capacities in the next few years. That will only happen if you build on existing knowledge. This is vital when it comes to scaling and automation, explains Tassilo Gast from automation specialist Emerson in his interview with H2-international.

H2-international: The hydrogen industry needs to grow extremely rapidly in the years ahead. What do companies, for example electrolyzer manufacturers, need to be especially aware of?

Gast: The electrolyzer projects that have been announced in the news are between 100 megawatts and 1 gigawatt in size. The electrolyzers installed up until now mostly have electrical capacities of 2 or 5 megawatts. That represents considerable growth and therefore a huge challenge for manufacturers.

Advertisements

Electrolyzers usually have a modular construction. For the most part, this principle still stands when they are scaled up, if only because of the physical and electrochemical limits on the size of the stacks. These days, stacks with around 2.5 megawatts of electrical capacity are commonplace. Even if a stack in the future were to be 10 megawatts, you would need 10 of them for a 100-megawatt electrolyzer, and hundreds of them for a gigawatt project. If I simply line up 10 modules side by side using the “scale up by numbering up” principle, then I have 10 times the number of interfaces, 10 times the number of cable ducts and so on. Wiring, balancing and controlling all that is highly complex. Consequently you have to rethink the system architecture.

If we take a large electrolyzer plant as an example – what would a successful scale-up with adapted system architecture look like?

The key thing is for someone to look at the overall system early on. In the case of Emerson, we have a dedicated business unit for systems. In theory, the manufacturers could also do it themselves, but they often just don’t have the capacity in the growth phase to take this step or return to this step and look at the overall picture.

Depending on the scaling factor, initially it can all be about taking small steps, for instance the merging of balancing groups. However, from a certain size, no later than several hundred megawatts, you have to build in a completely different way. At that point you can no longer install the modules in individual shipping containers, as you do for smaller plants – if only because the total cost of the containers would be too expensive. Instead, you build a plant with the stacks on a plot of land along with the accompanying plant units, for example for water treatment, as in greenfield projects. The electrolyzer would be planned in a similar way to a traditional chemical plant, on open ground – or under cover – with separate processing and plant sections. When we’re part of a process like that, it’s very important to work together closely. Together you have to take a long, hard look at the process so that you really manage to leverage the efficiency potential and cut down the time to market.

In addition to the redundancy of components and the spatial arrangement, are there other problems when scaling up that can be avoided with appropriate planning?

Yes, there are, for example in relation to safety. Hydrogen is, of course, an explosive gas. And the amount of gas increases as the plant size grows and this also increases the potential risk for surrounding areas. Equipment and fittings have to meet safety and disconnection guidelines; in the event of a fault, it must be possible to shut down safely. There is special software from AspenTech, which Emerson has owned since 2022, that helps to scale up a plant virtually, and indicates foreseeable bottlenecks and safety issues.

What role can a digital twin play in this kind of virtual scale-up?

The expression “digital twin” is used in lots of different ways. In its simplest form, it means a virtual map of the plant. The next step is to populate the digital map with data from the process in operation. This allows you to verify if the simulation tallies with reality. Emerson’s digital twins are able to verify data from the simulation with responses from field instruments and control elements from the field and thus preempt the behavior of the process. That’s immensely helpful, for example in the case of electrolyzer manufacturers or EPCs, when it’s all about assessing in advance the scaling effects of plants that are in the process of becoming larger. Finally, it enables better operational management – with higher efficiency, lower costs and longer component life.

Have you already delivered this kind of scale-up for an electrolyzer manufacturer so you can tell us about your experiences?

We have a lot of initial projects in the hydrogen sector around the globe. For instance, we’ve fitted out the world’s largest PEM electrolyzer plant with a control system, valves and instruments. It’s at Air Liquide in Bécancour, Canada. Emerson has also taken care of the integration into the on-site chemical process.

Here, we are able to draw on our know-how from other sectors. Regardless of which electrolyzer technology is being used – PEM, alkaline, AEM – scaled-up electrolyzers all need a lot of water, for example. The water has to be demineralized and conveyed to the electrolyzer and arrive there at the correct temperature and at the correct pressure. We take care of measuring all these factors, finding the right valves and fittings and controlling the process – from the electrolyzer, to gas separation and dehydration through gas analysis at the end to check the quality level of the hydrogen.

Stack production is essentially already highly automated. Bipolar plates are screwed automatically, for example. In some cases, Emerson components are used, for instance to place components in a certain position using compressed air.

Which companies in the hydrogen sector would also be interested in working with Emerson on automation or other improvements?

We’re active throughout the entire hydrogen value chain: in hydrogen production, in transportation and distribution as well as in our work with end users. An end user of hydrogen can be a large chemicals group, a steel group or a refinery, but equally a company from the papermaking, life sciences or cement industries. For example we have installed a system consisting of a large number of hydrogen refueling stations for an independent operator from South Korea. The operator now sees exactly how much hydrogen is needed at what time and at which refueling stations; it knows how many refueling operations take place, whether there are problems somewhere and what logistical measures it has to take to adjust its delivery logistics to meet requirements. These sorts of overarching control systems and system architectures for recording data and signals also play a role in large sector-coupling projects in which all steps can be monitored and aligned with each other – from the production of green power using wind or photovoltaics to hydrogen production by means of electrolysis through distribution via pipelines and refueling stations or to fuel cells.

In another instance, we have supplied a complete blending station for injecting hydrogen into the natural gas grid. Here, we worked together with a partner from the plant engineering industry. For a manufacturer of hydrogen plants and EPCs, that’s a big advantage. The manufacturer has a central point of contact for all aspects of automation that supplies everything from a single source. That’s not only much quicker but also brings the manufacturer a clear CAPEX benefit.

Is everything going quickly enough to cope with the ramp-up of the hydrogen industry?

For a successful ramp-up, all parts of the industry need to scale together. Silo thinking which is focused on individual plants or manufacturers is not helpful. When many electrolyzer manufacturers scale up, they simply do what they already know but increase the size and numbers. However, if you don’t adapt the system architecture, the CAPEX costs rise, and inefficiencies occur that just don’t need to exist. If you look into the general concept of automation at an early stage, aside from the development of new membranes or other research work, there is vast potential to reduce costs. To leverage this, you have to test out all manner of ideas and concepts early on and it needs an automation partner with a complete portfolio. Everyone has to be open with their partners as far as possible in order to identify potential together.

Can good automation in Germany and Europe enable us to stay competitive in hydrogen technology?

In Europe we have an incredible spectrum of companies and organizations from the hydrogen industry, especially in Germany. The technologies of these companies have a very high technology readiness level – plants are exported around the world. There are a lot of companies with a great deal of know-how. Even if staffing costs are higher here, that hardly has a bearing compared with other aspects. The problem has far more to do with regulation and policy. In the US, for example, there is the Inflation Reduction Act which provides a huge amount of support to companies if they create value in the US. It’s aimed particularly at companies in the environmental and sustainability sectors, such as manufacturers of hydrogen plants or subareas of the hydrogen value chain. It’s pointing the way for European industry, which means Europe must urgently readjust.

Another issue is that the approvals for projects and plants in Europe take far too long and are too diverse. A consistent regulatory framework would simplify a lot of things. It’s not just approvals that are time-consuming; other political commitments, such as funding and guidelines or targets, take an extremely long time in Europe. A case in point is the RED III Directive. The EU has now announced higher overall targets and updated the speed of the approvals procedure. Despite this, the procedures still take too long. If the hydrogen industry is expected to stay and scale up further in Europe and in Germany, then many things here have to become a lot faster.

Our interviewee:

Tassilo Gast is Emerging Market Business Development Manager for the DACH region (Germany, Austria, Switzerland) at Emerson. The company, which employs around 70,000 members of staff worldwide, specializes in automation solutions. Its offering includes hardware such as valves and measuring equipment, software for simulation and operational management as well as services including consultancy and design. In May 2022, Emerson acquired a majority stake in the company AspenTech, a specialist in process simulation software. Emerson works with customers in a wide variety of sectors, from breweries to refineries. The company also has many customers in the hydrogen industry. Its headquarters are in Saint Louis in the US state of Missouri.

About 20 years ago, solar power and Passivhaus design captured the imagination of one Polish couple. At the time, Dorota and Piotr Napierała regularly traveled to Freiburg in Germany where they got to know the pioneers of photovoltaic technology. “I got loads of ideas there. It was a time of awakening. We converged at trade fairs and exchanged our visions and ideas. There was a fantastic atmosphere,” enthuses Piotr Napierała. The Passivhaus concept in particular made a lasting impression on him. Today he continues to focus on the advantages of efficient microgrids and energy island solutions. “Put simply, it’s what excites me. On my Freiburg visits I enjoyed looking at the solutions from Hydrogenics and discussing them with the people there. I like small closed structures that I can optimize,” explains the physicist.

Advertisements

Virtud owners Dorota and Piotr Napierała have a clear goal: The annual energy costs of the Virtud hydrogen house should not exceed PLN 500, which is roughly equivalent to EUR 123. Piotr doesn’t set much store by grandiose projects and is also not convinced by the pumped-up hydrogen plans put forward by many well-known corporations. He believes that a lot can be achieved, especially when it comes to hydrogen, by taking multiple small, precisely tailored actions at a local level.

Huge potential in Polish PV sector

The Napierałas welcome their visiting business partners and prospective clients to a smart, white new build constructed on the Virtud premises in a suburb of Poznań. Now proprietors of a photovoltaic installation business, the husband and wife team have previously owned several companies within the renewables sector. Their specialization in PV technology began in 2015. The pair see the development of the Virtud hydrogen system as a logical continuation that will help spread renewable energy across world – and especially in Poland where the PV industry is currently booming.

At the end of January this year, the total installed capacity for PV plants in Germany’s eastern neighbor was over 12.5 gigawatts. In the previous year the figure was just 7.6 gigawatts. In other words, the photovoltaic capacity in Poland has almost doubled within 12 months. Consequently, solar power accounts for a good 54 percent of overall renewable energy capacity in Poland.

Car batteries store solar power

However, the massive increase in electricity generation from photovoltaics also brings enormous challenges for the industry. The main hurdle is how to store energy overnight and during the less sunny seasons of fall and winter.

Virtud has managed to solve these problems by taking an unusual approach. Instead of spending exorbitant sums on energy storage, for a relatively small outlay at auction the company bought large numbers of secondhand batteries that were previously used in Nissan Leaf cars, a popular model in Poland. The batteries are combined into packs that store solar power produced during the day, allowing it to be released again at nighttime. Piotr Napierała reckons that the solution including the electric car batteries costs only a twelfth of the price of a new energy storage solution.

For those wanting to bridge the fluctuations between the summer and winter months, batteries alone will not suffice. This is where hydrogen comes in. “We use the sun and wind to produce green hydrogen which acts as the energy carrier at those times of year when demand is highest,” the entrepreneur says.

Evolution of the energy sector

The Napierałas are certain that the renewables sector will continue to evolve and that hydrogen is merely a logical step. As businesspeople, they have been involved in many stages of the renewable energy trend and have repeatedly noticed how dynamic the process is. This also applies to the bureaucratic and legal sides, as Dorota Napierała remarks. She is responsible for all approvals and application requests in the company. “We have a long learning journey ahead of us with regard to hydrogen,” she says.

Recent decades have seen the introduction of many highly complex renewables laws in Poland. Electricity feed-in to the grid was made possible in 2014. This was a completely new world in terms of accounting and administration. Dorota Napierała spent a great deal of time in meetings and on the phone to the relevant authorities until both sides fully took the new legislation on board. “It’s always a learning process. We learn from each other. It will be similar with hydrogen. The authorities have become much more open now. If there are any queries or uncertainty, they actually phone up and you go through the forms again. For years we’ve been part of a two-sided education and communication process. That makes everything easier,” Dorota Napierała explains.

A model for the future

Looking around the show house, an energy-efficient 200-square-meter (2,150-square-feet) building, it’s not just the use of solar power and a heat pump that is noticeable. The large area to the right of the entrance also catches the eye. This is where the 2.4-kilowatt electrolyzer is located. Supplied by German manufacturer Enapter, it’s the first electrolyzer installed by Piotr Napierała. “Many, many more are due to follow,” says the co-proprietor. Other technical kit is also housed in the modular cabinet, including water purification equipment. But there is still enough room for additional electrolyzers.

Access is currently being created from the demonstration area to the hydrogen tank, which is already on order. This will make it possible to refuel vehicles with hydrogen. That’s the next job on Piotr Napierała’s list.

For a long time the public has held a deep fascination for solar power and hydrogen. Around the world, both of these technologies have been described as great opportunities and the solution to our energy problems. Indeed, hydrogen is regarded within the current public debate as a cure for all ills. What’s the latest on these solutions? Where does the green power they need come from? And how can (green) hydrogen and photovoltaics more rapidly leverage their huge shared potential?

Advertisements

When we started designing and building solar power plants in 1992, the fascination with hydrogen and solar energy was already immense. However, photovoltaic or PV plants were extremely expensive. In Germany they were only bought by enthusiasts, and even these purchases were dependent on (massive) grants. These (lost) grants came and went, just as the new pilot schemes and flagship projects did. The only relatively stable markets to be found globally were in space flight (no concern about cost) and off-grid, where suitable. Grid-connected photovoltaics didn’t make much progress in terms of scaling up production, and therefore the plants remained expensive and practically irrelevant for energy supply purposes.

In 2000 (global PV market then: 200 megawatts), photovoltaics started to evolve into a mass-use technology, a development that was largely down to the huge international boost provided by Germany’s renewable energy law EEG. In 2023, the global market is expected to reach 380 gigawatts of new installations. The electricity generated around the world by this newly installed capacity would be enough to cover Germany’s current electricity demand.

PV plants have the lowest power-generating costs of all new facilities. These costs have fallen by 95 percent since 2000. It is anticipated that the global PV market will grow tenfold by 2035 – accompanied by further efficiency increases and cost reductions. All this has been made possible through the creation of a market in the earlier stages that can also now in Germany generate solar power without the need for any subsidies.

In our view, we don’t yet have a comparable approach to confidently realize those same (necessary) scaling effects in the hydrogen sector in a way that provides planning certainty for industry. That said, there are hydrogen regions, pilot projects and initial marketplaces springing up all over the place and there is a great deal of goodwill within politics and the media. But when it comes to the market for new hydrogen, things quickly become difficult or just downright impossible. It’s no wonder that large off-takers (e.g., steelworks that have started the conversion to hydrogen) as well as small- and medium-size enterprises are hesitant about purchasing hydrogen, if they are indeed interested at all.

Some can’t get sufficient quantities; others don’t want to pay today’s high prices. For the expectation is that hydrogen will get cheaper. Plus, virtually every day that passes there are fantasies of some – unrealistic – hydrogen import. Or of a bridging technology: blue hydrogen with carbon capture and storage. But nobody has yet stuck a price tag on these potential sources.

The massive success of photovoltaics was previously in having solved this chicken-and-the-egg problem through the EEG. Each energy producer (regardless of size) had a guaranteed off-take over the required payback period along with a price guarantee. Electricity buyers, on the other hand, paid the relevant market prices. As the support scheme was highly degressive, the desired cost reduction was taken into account or given a huge push.

These days, this form of support is barely needed, if at all, and in many areas and countries it is now being aligned with market conditions through the process of tendering. Similar systems for ramping up hydrogen are under discussion in the European Union or are being announced in the form of EU tenders. Just as in the solar and wind industries, contracts for difference or CFDs could be introduced for hydrogen with the establishment of hydrogen exchange prices as a reference point.

Why is that a key issue?

Whoever invests in an electrolyzer (together with storage etc.) can be certain that much cheaper and more efficient equipment will be available to purchase in three to five years’ time. Reliability will also have improved. It’s thus foreseeable that both CAPEX and OPEX, or put more simply, the price per kilogram of hydrogen, will decrease massively. Unless there is a guaranteed off-take at the price needed today, the project quickly becomes bankrupt.

By contrast, the hydrogen buyer from a steelworks or indeed from a municipal energy supplier, for example, will surely refuse to sign a long-term hydrogen purchasing agreement right now when it’s clear that prices will fall massively in the coming years. If an attempt is made to get around this, e.g., through “lost” subsidies or one-off grants, there is the possible threat that, after these measures have been applied, bankruptcy will occur or the electrolyzer will be shut down since the support is indeed “lost.”

What’s more, this type of approach has in the past proved to be highly difficult to get right in terms of how the support is structured. But more than anything, it has always been dependent on the particular budgetary situation of the funding organization.

A “hydrogen CFD” or a similar instrument can incentivize a diverse range of players and also encourage rapid market expansion as well as a quicker pace of innovation.

Application assumptions

If 15 years ago hydrogen-driven cars were the only promising technology for real distances over 100 kilometers (60 miles), then the technological evolution of battery storage has now already superseded this, i.e., prior to mass use. And this has happened despite the fact that the development of battery-based vehicles and their batteries is in its infancy.

By as early as 2025, Germany, too, is likely to witness the price of battery electric vehicles dropping below that of their combustion engine counterparts. Whether you like this reality or not, that proverbial ship has already sailed. If you also take a look at the trend for trucks, the race here will likewise go in favor of batteries.

How things will pan out for commercial vehicles or rolling stock remains to be seen. However, all these categories have a powerful competitor in the form of hundreds of millions of new batteries that are coming on the market globally every year. That’s because these batteries also cushion the grids and make “mass charging” possible. And railroad electrification using common overhead wires is also another real rival when it comes to purchasing and operational costs, as a battery or hydrogen train is not an end in itself.

In my opinion it’s important not to hold onto applications that simply have no real chance of making it big, since it just frustrates people when these promised technologies don’t then materialize. What’s more, using hydrogen for heating in ancient condensing boilers is so nonsensical and expensive that the hydrogen sector should, as a matter of urgency, distance itself from the natural gas sector, which has been pushing this very agenda, so that it can maintain its own credibility and, above all, control the narrative around its own technology.

Applications such as the production of hydrogen-based aviation gasoline or marine fuels and all the other fuel applications as well as hydrogen storage applications – an aspect that desperately needs redefining – are such an enormous future market that there is no need to lament it.

Why do hydrogen storage applications need to be redefined?

In the various long-term scenarios presented to governments by research institutes, there isn’t a single scenario which reckons on the already burgeoning wave of millions of (bidirectional) energy stores in vehicles and the already highly cost-effective medium and large decentralized energy stores. From 2024, no solar farm will be built in Germany that doesn’t have its own storage facility to allow power to be sold at night – and that’s without the need for any funding.

Millions of smaller energy stores are being set up too and these are all significantly extending the actual grid options on offer locally. International developments are taking place at a much faster pace than they once did for PV. Battery storage is making solar energy available “during the night” and “bringing wind to windless days” – for a few hours, then days, then weeks. And this mass availability costs just a few euro cent per kilowatt-hour. This will considerably change all previous scenarios outlined for hydrogen’s use as an energy store.

Off-grid also an option

Hydrogen can also be produced off-grid on a gigawatt scale, provided it is possible to transport the product (hydrogen or an e-fuel) reliably and at a reasonable cost. This is an extremely interesting aspect that is achievable all over the world, with differing proportions of solar and wind power (or, where feasible, other renewable sources). These forms of renewable generation complement each other locally and can, with back-up storage, enable very high running times for electrolysis without costly and time-consuming connection to the power grid. Since their end product is not electricity but hydrogen-based substances. Projects along these lines are happening in various countries, and this has become a realistic option for Germany as well.

Distancing from costly “bridging technologies”

There is a serious ongoing discussion within associations and the media about carbon capture and storage, otherwise known as CCS, and its use in Germany as a bridging technology to obtain blue hydrogen from natural gas by the start of the 2030s. In this case, a technology that is still at the prototype stage after decades of political discussion is being pushed onto a totally unfeasible timeline. And that’s without any discussion of the overall costs of such an option, assuming that (at some point) it is indeed available for large-scale deployment.

Ultimately, CCS has been repeatedly sold as an option for coal power plants since the 2000s and has never come to fruition – for cost reasons. Plus, with such ideas, all the problems of security of supply, costs and the finiteness of natural gas still remain. CCS is a dangerous, insubstantial distraction from the long-term and quickly scalable technology pathway of renewable electrolysis in the EU.

Underrated opportunities

Hardly a day goes by when there isn’t a public discussion of all manner of ideas for the hydrogen economy. It almost doesn’t matter where the German Chancellor or the minister is traveling, it’s nearly always about importing hydrogen. And of course it’s hydrogen at a “bargain price,” with a total absence of debate about the costs or prices. It’s already the case today that a veil is drawn over the massive existing political tensions and risks of potential supplier countries. In fact it’s terrifying how little discussion there is in political and media environments about the EU’s own potential and, especially, the cost of hydrogen options. That’s why I want to make a simple “back-of-the-envelope” comparison, taking into consideration hydrogen minimum costs:

If I want to produce hydrogen “in the desert,” I have to…

– pay (higher) costs than in the EU for electrolyzers, plant engineering, security etc.

– desalinate seawater (CAPEX costs and electricity consumption).

– use wind and solar power at a minimum cost of 1.5 euro cent/kWh, with battery stabilization for high electrolyzer utilization levels on top, albeit the prices will generally be above the costs.

– calculate the losses due to waste heat (20 percent to 40 percent of the electricity used) since the thermal energy will not be used in the local climate.

– calculate the expense of equipment such as the compressors for transportation.

– assess the costs of the pipeline or tanker and their losses in operation.

– adopt a calculated risk strategy for unstable regions.

– …

If I want to produce hydrogen in Germany or in the EU, I have to…

– pay lower costs than in the desert for electrolyzers, plant engineering, security etc.

– pay for water.

– use wind and solar power at a cost of 4 to 7 euro cent/kWh, plus a bit more for stabilization, whereby avoided curtailments from the power grid can lower the price.

– transfer waste heat for the purposes of district heating or process heat. Then I would have 20 percent to 40 percent lower electricity costs because this can be sold as heat – or equally “written off.”

– calculate the expense of equipment such as the compressors for transportation.

– ensure direct consumption locally or short tanker/pipeline routes (lower losses and costs).

– dispense with the need for a risk strategy for unstable regions.

– …

Finally, I think it would be necessary to refine the above back-of-the-envelope calculation by inserting real figures that take into account the expected massive decline in cost. First and foremost, this would enable realistic assessments to be made (at last) about what green hydrogen can cost in 2030/2040 and which prices are reached based on it – in the EU and beyond – thus staying well clear of outlandish buzz phrases like “hydrogen is the Champagne of the energy transition” or “hydrogen will make heating affordable.”

Landesmesse Stuttgart has put the industry event just renamed Hy-Fcell on course for growth. In view of increasing global competition in the event segment, the trade fair company was working towards establishing Stuttgart as an international nucleus for especially the fuel cell vehicle sector. On September 13 and 14, more than 150 exhibitors presented their products and services at the fairgrounds by the airport – this year in Hall 4 for the first time, directly behind International Congresscenter Stuttgart (ICS).

The kick-off was being made this year by Daria Nochevnik, director of the Hydrogen Council. As head of this worldwide association of hydrogen activists, she lookd at the H2 economy on a global level in her keynote. She said: “Germany has from the start played an important role in the introduction of the hydrogen economy in Europe and on a global scale.”

Advertisements

Invited as well were political representatives like Baden-Württemberg’s minister for environment and energy economy Thekla Walker as well as parliamentary secretary in the federal ministry for economy and climate protection Dr. Franziska Brantner. At the conference were 60 expert presentations focused on fuel cell production, where the research platform H2GO of the Fraunhofer institutes hold alone eight sessions. Further talks were also offered by – in addition to the hosting Hy-Fcell team – the administrative agencies for hydrogen NOW, e-mobil BW, VDMA, DVGW and ZSW.

After a long time, vehicles with alternative drives were once again shown off and offered for test drives. New were also the hy-fcell Technical Tours, which provided an exclusive behind-the-scenes look at local industry players. In guided tours, various buses started from the fairgrounds and went to manufacturer Cellcentric and state research institute Zentrum für Sonnenenergie- und Wasserstoff-Forschung Baden-Württemberg during Tour Ulm. Tour Heilbronn leaded to German aerospace agency location DLR Lampoldshausen as well as to the Audi location in Heilbronn. And during Tour Stuttgart, public transport company SSB as well as Hydrogen Green were viewed.

Katharina Jathe, director for Hy-Fcell at Messe Stuttgart, stated, the Technical Tours not only promised “exciting inside views into the work of pioneers in the field of hydrogen and fuel cell technology”, but also granted a “special view of Region Stuttgart”.

COMPREHENSIVE OFFER

Particular attention was placed on startups this time. In a central area, startup companies from various countries introduced themselves, met potential interested parties and also established new business relationships. Stefan Lohnert, managing director of Messe Stuttgart, said regarding this: “The industry thrives on brave and visionary people.” That is why we wanted to give young entrepreneurs a “stage of their own and offer them an opportunity to transform their ideas into profitable applications”.

In addition, a Speakers Corner was set up in International Congresscenter Stuttgart on the fairgrounds, and a B2B Matchmaking as well as a Networking Night was offered. There was also something for up-and-coming or, conversely, established professionals: During hy-fcell Career Compass, businesses presented themselves in 3-minute pitches. In a subsequent speed networking session, potential associates could find each other in a more direct fashion.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.