by Sven Jösting | Apr 17, 2024 | Fuel cells, international, News, Stock market, worldwide

Hyzon Motors will start production of 200‑kW modules for commercial vehicles in the USA in the second half of 2024. This should then lead to a recovery of the strongly depressed share price via incoming orders. Parallel to this are running product presentations such as the recent one in Melbourne (Australia) with the 200‑kW Hyzon Prime Mover at the Kangan Institute Automotive Centre of Excellence. Deliveries in New Zealand, Australia, Europe and the USA are planned for later in the year. This fuel cell system can be used in many other applications and markets at the same time: rail vehicles, maritime transport, stationary energy, mining vehicles, etc. It will be interesting to see which customers this 200‑kW single stack will find and the order potential that will result, especially as it offers a cost reduction potential of over 25 percent and conserves 30 percent of the space and weight – compared with a 110‑kW system. A first major market for Hyzon will be the employment in commercial vehicles in Australia, where the company has an important location with around 50 employees.

Patent registrations – Competition with Toyota and Bosch

Advertisements

Hyzon Motors has applied for a number of patents in the USA, Europe and Asia and many have already been granted. The main focus here is on reducing emissions when using fuel cells, but also on battery systems. What this means in detail is not clear to me, but shows that Hyzon is very active in securing patents and sees in it an important basis for its FC products and utilizations as well as markets. This would put them in direct competition with companies such as Toyota and Bosch. This could – purely theoretically – eventually lead to license revenue.

Hyzon still has with over 100 million USD sufficient capital, but will not be able to avoid taking measures (issue of new shares or participation of a strategic investor) to finance the company’s growth and expansion. The production facility in Illinois is self-financed. Production ramp-up is beginning in the second half of the year. Incoming orders for the FC modules as well as speculation by a strategic partner or investor make the share of Hyzon Motors a very interesting speculation, although the investment is to be classified as highly speculative as you’re dealing with a start-up.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: Sven Jösting, written March 15th, 2024

by Sven Jösting | Apr 17, 2024 | Fuel cells, hydrogen development, News, Stock market

FuelCell Energy has with SOFC fuel cell power plants built its own capacities for clean energy totaling 62.8 MW (previous year: 43.7 MW). The company’s own high-temperature fuel cell serves as the basis for use in electrolysis, where the company has recognized great potential for itself. Along with that are various research projects, among others in Canada, and the company relies on specially developed carbon capture technology that is designed to avoid emissions and generate emissions-free energy at the same time. So far, so good. But you can’t avoid thinking of competitors such as Bloom Energy, Sunfire and Ceres Power (indirectly also Weichai Power and Bosch), which pursue similar visions and technological approaches to FuelCell Energy.

What all this means in terms of order and implementation potential is unfortunately not yet clear to me. The figures so far are sobering: The first quarter (fiscal year 31.01.24) brought a loss of 44.4 million USD. Turnover fell in the quarter to 16.7 million USD. Of liquidity, the company has no lack: 348.4 million USD was in the bank January 31, 2024. However, there has been a constant outflow of capital for years, aided by constant share placements on the stock exchange via an ATM program. Projects such as that with Exxon in Holland sound promising, but say very little about the potential. In South Korea, former partner Posco, via its subsidiary Korea Fuel Cells, forfeited the option of further orders in supplement to a previous project. Not a good sign.

Advertisements

Joint venture with ExxonMobil

At first glance, it sounds promising: FuelCell Energy and ExxonMobil have agreed to build a production plant for carbon capture in Rotterdam. It entails the avoidance of CO2 emissions or the storage and making usable, without generating a carbon footprint. CCS stands for carbon capture and storage. After successful deployment directly in the neighborhood of important industries, the project that is based on the technology of FuelCell Energy could be deployed at all production sites of ExxonMobil where CO2 emissions are generated. The process is to generate heat as a by-product and enable the production of green hydrogen.

Unfortunately, there is no indication of the exact investment volume (invest on the part of FuelCell Energy) and the order volume that can be derived from this. In any case, the project is financially supported by the EU via the Emissions Trading System Innovation Fund. ExxonMobil and FuelCell Energy have already been working on the associated technologies for some time, so this specific project represents another important milestone.

The cash cushion is safeguarding the share price well. The stock exchange will rediscover FuelCell Energy when it can be shown how technologies such as carbon capture and SOEC can generate orders and earn money. That will take some time. The share is always suitable for trading, as good news quickly leads to major price swings.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: Sven Jösting, written March 15th, 2024

by Niels Hendrik Petersen | Mar 18, 2024 | Development, Energy storage, Europe, Germany

Interview with Thomas Korn, CEO of water stuff & sun

Startup company water stuff & sun has developed a novel technology that is designed to provide a safe and easy way to store hydrogen. The solution’s key component is its microvalve system. A pressure regulator controls the release of hydrogen progressively from 1,000 bar down to just a few bar. H2-international spoke to Thomas Korn, CEO of water stuff & sun, about how it works and the challenges encountered.

H2-international: Mr. Korn, the storage and refueling of hydrogen is a challenging issue. How do you solve that problem?

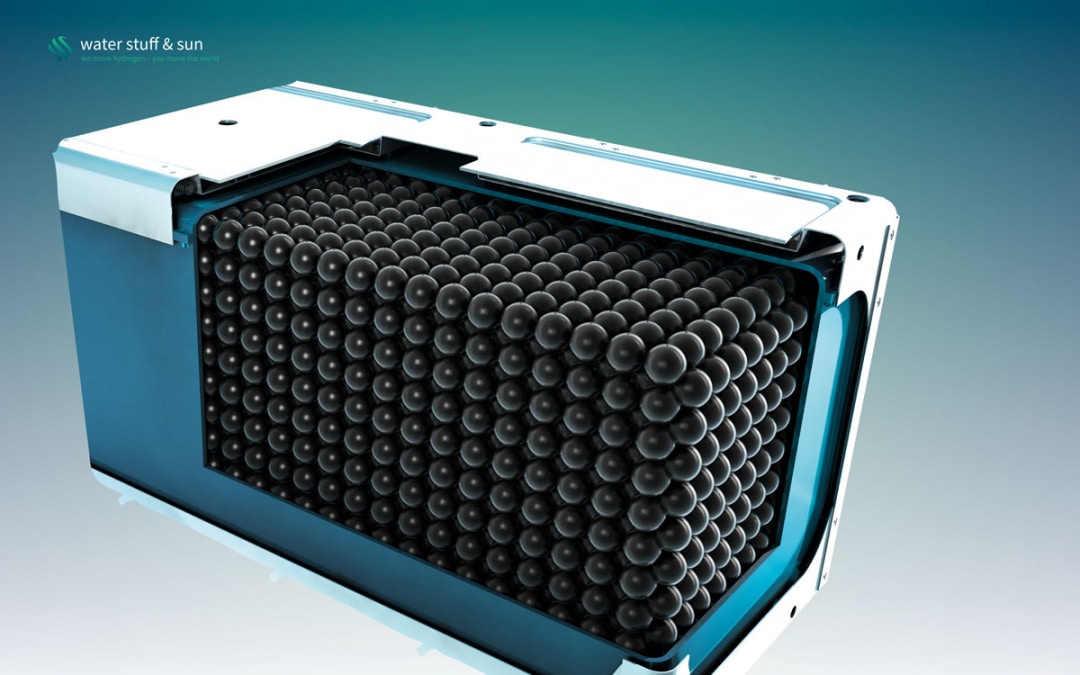

Korn: As it stands, the storage of hydrogen in conventional compressed gas tanks is complex and expensive. There is a trade-off between performance, safety and cost. We have a surprising solution to this: Instead of using a small number of large cylindrical tanks, our technology allows us to store the same amount of hydrogen in multiple spherical carbon-fiber vessels the size of a tennis ball. The silicon microvalve system, which is built into every pressurized ball, means that all the vessels act identically and in unison, just like a large tank. The expense involved in ensuring the safety of hydrogen stores can be significantly reduced if the energy is split into multiple small vessels. As a result, we save almost half the carbon fiber material compared with a standard pressurized tank. We call these ball-shaped high-pressure storage vessels Sfeers.

Advertisements

They allow hydrogen cells to be scaled as required and integrated into hydrogen batteries of any shape. Green hydrogen can thus be used in a variety of motive and stationary applications such as trucks, drones and airplanes. The next generation of these energy stores will be 95 percent lighter and up to 30 times cheaper than lithium ion batteries – while still carrying the same amount of energy.

Fig. 2: Doing the rounds: a Sfeer ball at the EES trade fair in Munich

How does the hydrogen battery work?

Hydrogen batteries are low-pressure hydrogen tanks containing Sfeers which are filled at up to 1,000 bar. The hydrogen battery enclosures are designed for low pressures and can therefore be perfectly adapted to the available installation spaces in a wide array of mobility products. When hydrogen is extracted, the pressure in the hydrogen battery enclosure decreases and activates the microvalve system in all the Sfeers once the pressure drops below a mechanically programmed ambient pressure range. These then release hydrogen, together providing the energy required for a hydrogen engine or a fuel cell.

The pressure in the hydrogen battery rises again above the pressure activation level that is set during the manufacture of the micromechanical components. Once the pressure level has been reached, all the microvalves close. The pressure in the battery stays constant or reduces further if the consumer withdraws more hydrogen. The activation pressure is set to the supply pressure of the consumers. The hydrogen battery can be thought of as a low-pressure tank, but with the capacity of a high-pressure tank.

The concept increases the safety level while at the same time reducing the amount of material used. Since their highly adaptable shape means they can make best possible use of the available space, hydrogen batteries outperform conventional pressurized tanks in terms of volumetric and gravimetric power density.

Microvalve technology has its origins in satellite technology. How is this technology produced?

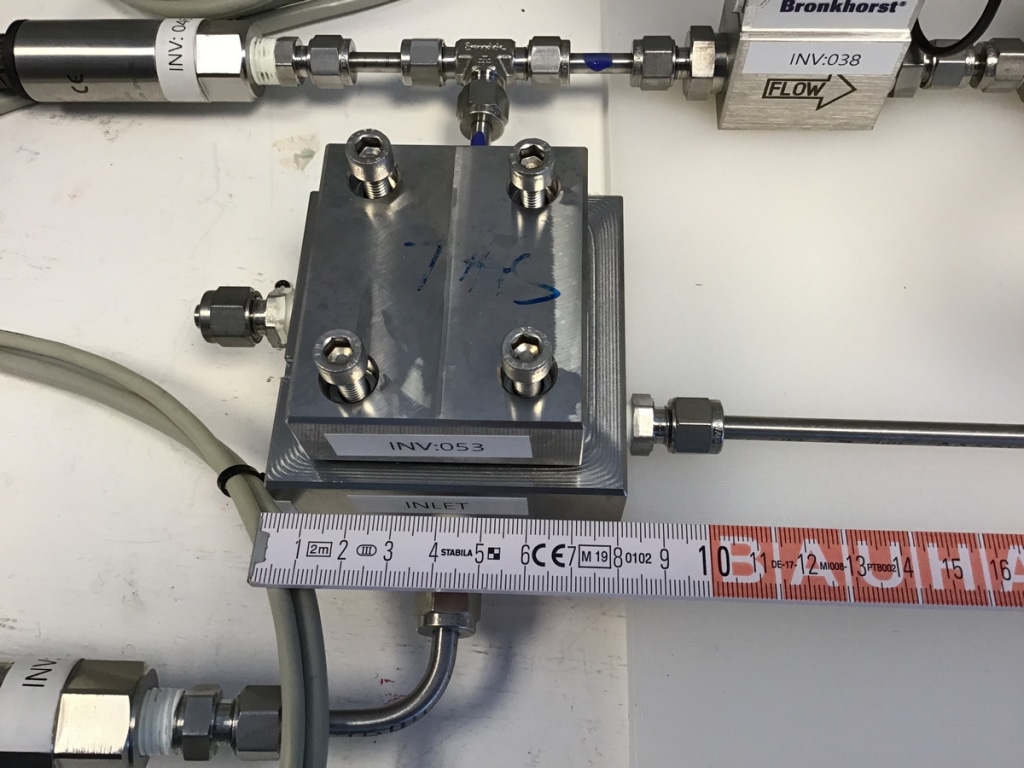

Satellites have a gas propulsion system that secures their position within the communication window. Even in the early days, industrial developers started to use microsystem technology to regulate gases due to financial pressure to make ever smaller and lighter satellites. Our innovation centers on the development of micromechanical switching elements that don’t need electrical energy for their control; instead they are controlled passively by the ambient pressure. As in semiconductor engineering, highly industrialized manufacturing processes are used that can create thousands of identical parts on large silicon wafers. Valves, gas channels and the five-stage pressure regulator are produced and joined in four silicon layers. All chip components are built into a space measuring 4 x 4 x 2.5 millimeters (0.16 x 0.16 x 0.1 inches).

How did you come up with the idea of spherical high-pressure vessels?

The technology was invented by Prof. Lars Stenmark, who taught microsystem engineering in the Ångström Laboratory at Uppsala University and who had already applied earlier inventions to the aerospace industry. When he told me about his hydrogen storage invention, I was all for it. A physical hydrogen storage vessel that combines two existing technologies and resolves the trade-off between safety, cost and performance in hydrogen tanks – we couldn’t resist and founded the company water stuff & sun in January 2017.

Fig. 3: A view of the lab shows the test setup for microchip evaluation

Is there already a prototype?

We have already produced and tested prototypes of switching valves and the key element of the valve system – the pressure regulator – in the clean room of the Ångström lab in Uppsala. We have also put a carbon fiber Sfeer prototype through a burst test and validated our simulation model with the results. At the moment we are building the first system prototype of a hydrogen battery with three Sfeer cells. The prototype and its use in a micromobility application will reach technology readiness level 5 in the first half of 2024. At that point we’ll start to develop hydrogen batteries for specific mobility products with several manufacturers and go on to industrialize them in the next stage. There is a great deal of interest from industry. For example, we have already submitted a joint funding project with an aircraft manufacturer and the German Aerospace Center. We are working with our partner Keyou to develop hydrogen batteries for converting and retrofitting trucks and buses. Additionally, we’ve managed to stimulate interest from a mining machinery manufacturer and a truck OEM.

Returning to the refueling process: Am I right that you are intending to swap the tanks?

Hydrogen batteries don’t need to be refueled in the vehicle; they are exchanged at swap stations or, in the case of small applications, they can also be exchanged by hand. That way, refueling can take place quickly and cost-effectively. The empty hydrogen batteries are refilled at central compressor stations and returned to the swap stations. The low operating pressure and the limited quantity of H2 in the hydrogen battery enclosure makes this ease of handling possible. In comparison with conventional high-pressure or liquid hydrogen refueling stations, the expense and complexity are significantly reduced, which in turn lowers the capital and operating costs and thereby also the hydrogen price. For heavy-duty vehicles, for instance, with hydrogen, several hundred liters of fuel energy equivalent need to be compressed, cooled and transferred. By simply swapping the hydrogen battery, the process can be completed in just a few minutes.

The financing required will be considerable. What are the next steps for your company?

The need for capital in a tech startup is always an issue – it’s a continuous process. We have just started a new financing round in which our existing investment partners, such as the investment arm of Kreissparkasse Esslingen-Nürtingen, or ES Kapital for short, the company Besto, run by the entrepreneurial Beyer and Stoll families, and machinery and tooling factory Nagel, have already registered an interest. I would refer to them as relatively down-to-earth, regional investors that have been involved from an early stage. The plan is to invest the new cash in the development of a prototype in the motive application area, as mentioned earlier, among other things. The raw materials for the production of semiconductor chips are all affordable. Carbon fiber and silicon are readily available on the market. That is an advantage in terms of further scaling. If everything goes according to plan, we will see the first of our batteries in a vehicle or aircraft by 2025.

Fig. 4: The H2 battery should be quick and easy to swap in and out of a truck

When and how will the market for your solution evolve?

The transformation of energy systems is well under way. Infrastructure for natural gas- and oil-based fuels is being replaced by hydrogen and liquid hydrogen derivatives such as ammonia, methanol or synthetic fuels. The competition for technology leadership and, ultimately, energy leadership began long ago. In China and the USA, many billions of euros are now being invested in hydrogen technologies and their infrastructure; we Europeans are attempting to counter this with the Green Deal. Hydrogen projects are sprouting up all over the place. As far as we are concerned, the market has already started; we’re currently concluding cooperation agreements with initial vehicle and machinery manufacturers.

Where will the first market be that manages to develop?

We need to take a multitrack approach and are therefore also looking at the USA and the Arab world. The country that achieves the lowest hydrogen prices by investing will attract a lot of companies and investment. In the EU and Germany I hope that the greenhouse gas quota gives us an instrument that is competitive.

You won a prize at the World CleanTech StartUPs Awards, otherwise known as WCSA 2023. What particularly impressed the judges?

Firstly, the award as a platform is a very interesting network in itself. Applications for WCSA 2023 were invited by ACWA Power in strategic partnership with Dii Desert Energy and the French institute for solar energy CEA-INES, among others. The judging panel recognized the transformative potential of the hydrogen battery. The innovation could create an efficient and flexible infrastructure for H2. The electricity costs for hydrogen production from renewables are very low in Dubai. That’s why ACWA invited us again at the end of 2023 to present our solution locally. That will be extremely exciting.

In November we received two awards at the Global EnergyTech Awards: the prize for the Best CleanTech Solution for Energy and a special prize for Best Stand Out Performer. We were the only winners from Germany. That helps.

Interviewer: Niels Hendrik Petersen

Fig. 5: Thomas Korn

Thomas Korn has been working in the hydrogen field since 1998. The engineer’s experience includes work at BMW on fuel cell development. In 2015, he co-founded the hydrogen startup Keyou in Munich. The startup water stuff & sun was launched in 2017 in Unterschleißheim, Bavaria. The fledgling company now has 15 members of staff and a branch in Uppsala, Sweden.

by Hydrogeit | Mar 15, 2024 | Development, Europe, international, News

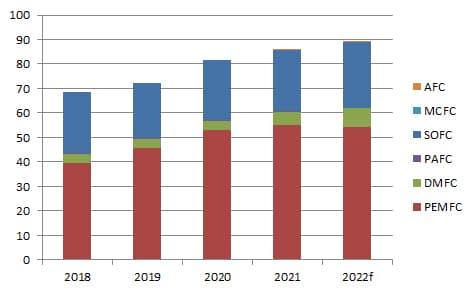

Fuel Cell Industry Review 2022

Year 2022 saw fuel cell shipments creep up over 2021 numbers, though the latter was a remarkable year. When 2021 exceeded 2020’s MW numbers by over 70%, we thought we were finally seeing the uptick that had been anticipated – the classic “hockey stick” pattern. But the structure of the industry – and its reliance on only a few players for the majority of shipments – means that growth comes in spurts.

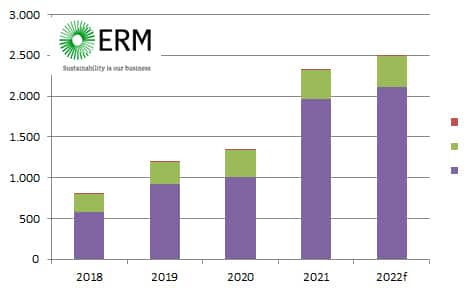

E4tech’s eighth annual Fuel Cell Industry Review showed just under 86,000 units shipped in 2021, or just over 2,300 MW, even with the COVID pandemic still hanging over markets. But this rapid growth was largely due to the activities of two vehicle OEMs, Hyundai and Toyota, together accounting for over 70% of the megawatts. But even after taking these out of the picture, growth continues – slowly but surely.

Advertisements

E4tech is now part of ERM and the team is continuing to research and write the Review. The ninth FCIR shows that 2022 shipments were similar to the year before – with the continued but slow growth still led by Hyundai and Toyota, at over 60% of MW shipments, and by fuel cell buses and trucks into China. In 2022, we estimate nearly 89,200 fuel cells to have been shipped, amounting to almost 2,500 MW.

Analysis by region

For vehicles (which by far is the largest contribution, at 85% of all shipments by megawatts), much of the demand was localized to China and South Korea. China saw over 4,150 units being shipped, across all modes of mobility (including forklifts, now slowly taking off in the country), while South Korea saw nearly 10,400 deployments, dominated by Hyundai’s Nexo. Together with 831 Toyota Mirais going into the home market of Japan, Asia now accounts for around 15,600 units into transportation markets, or 17% of global shipments of fuel cells by number, but rather more impressively some 1,500 MW (60%) of the shipped megawatt count.

Hyundai is benefitting from the 50% subsidy for fuel cell vehicles in South Korea. South Korea is now also the single largest market for large stationary units, in CHP and prime power modes. Stationary shipments into the country grew from 147 MW in 2021 to 196 MW in 2022 (8% of the global MW count). These numbers illustrate the importance of South Korea for fuel cell shipments – and, moreover, the key role of sustained policy and subsidies in helping fuel cell companies and OEMs to achieve volume.

In context of the Japan’s Ene-Farm program, across all markets (stationary, mobility and portable), Asia accounts for 60,850 units (two-thirds of global shipments) and 1,770 MW (71% of global shipments). Behind Asia is North America, with around 14,550 fuel cell shipments (nearly 485 MW, or 19% of global shipments in megawatts), led by Toyota and Bloom Energy shipments to the United States. Europe accounted for roughly 13,250 of fuel cell shipments in 2022, down from just over 14,000 units in 2021. The fall in unit shipments followed the completion of the PACE program of the US Inflation Reduction Act and the imminent closure of KfW-433 grant funding by Germany. In megawatts, the count slightly increased, from a corrected 204 MW in 2021 to 228 MW in 2022, about 9% of the global market. Fuel cell vehicle shipments to Europe are lower than for Asia and the US because of the low subsidies provided by the national governments.

Analysis by application

Fuel cells for mobility, primarily cars, continued to dominate the overall count. Across all modes of mobility (including forklifts), 85% of shipments (2,100 MW) fell into this category in 2022, 150 MW more than in 2021. In units, mobility accounted for 35% of shipments in 2022, a slight fall from 2021’s share. So, the message is transportation is growing, but other fuel cell markets are growing too.

The next main contributor to vehicle shipments is China, with a record 3,789 units (buses and trucks) being shipped over 2022. Together, these are estimated as contributing 387 MW to the overall count in 2022.

While nearly 1,000 fuel cell buses were shipped into China in 2022, fewer came to Europe in 2022 (only 99 registrations). According to CALSTART figures, as many as 82 new fuel cell buses were fielded in the US in 2022, mostly in California. Outside China, fuel cell truck shipments globally in 2022 remained minuscule. This could change, given the business plans of Cellcentric, Plastic Omnium, Hyzon and others.

Fuel cells for ships and for aviation remains exploratory, now with a growing emphasis on propulsion rather than hotel loads or auxiliary power. Forklifts continue to be a major application for fuel cells, albeit with fewer unit shipments in 2022 (over 9,650 units) compared to 2021 (over 13,400 units). Prime power and CHP comprise a large part of the remaining demand, in unit numbers and in MW. By number, micro-CHP still dominates, with Japan leading with its Ene-Farm program. ACE shows 42,877 units being installed in 2022, over 3,000 units more than the previous year. Outside Japan and Europe, micro-CHP shipped in negligible numbers, further demonstrating the criticality of country-to-country policy in supporting fuel cells. Together, prime power and CHP across the power range contributed 364 MW shipments in 2022, up from 335 MW in 2021. Although a growing emphasis for developers, fuel cells for grid support and off-grid power has remained subdued, at 14 MW (for both years). Shipments of portable fuel cells (including smaller ported APUs, less than 20 kW in power output) showed an increase, from just over 6,000 units in 2021 to nearly 8,000 units in 2022. These are supplied globally, but most feed into European and North American industrial and consumer markets.

Shipments by fuel cell type

PEM continues to outweigh other fuel cell types in shipments, both in volume and in MW capacity. Of the nearly 90,500 fuel cells shipped in 2022, over 55,000 were PEM. By megawatts, PEM fuel cells recorded 2,151 MW, 86% of the overall volume of shipments.

High-temperature PEM, generally utilizing methanol rather than hydrogen as a fuel, continues to grow, led by Advent Technologies. While still a fraction of overall PEM units at present, shipments are set to grow more aggressively given the improved logistics and increased runtimes enabled by the methanol fuel. DMFC (direct methanol) had a good year, with nearly 8,000 units shipped over 2022, mostly from SFC Energy.

SOFC (solid oxide) grew to nearly 27,000 units in 2022 (mostly micro-CHP, by number). The MW count grew from 207 MW in 2021 to 249 MW in 2022. Much of this is attributable to stronger sales from Bloom Energy. PAFC (phosphoric acid fuel cell) shipments fell, and while no new MCFC (molten carbonate) system placements were recorded over 2022, FuelCell Energy continues to produce significant volumes of stacks, for mid-life refurbishment of systems. AFC (alkaline) shipments increased to over 100 units in 2022, way down on other fuel cell types despite the lower cost potential, both for the fuel cell stack and the hydrogen purity requirement.

Summary

Fuel cells had a good year in 2022. Despite shipments being dominated by a few key suppliers into just a few countries, we are at last beginning to see shipments into Australia and South America, buoyed by the greater interest in hydrogen generally. And while interest is helpful, it remains the case that fuel cells have yet to break through the high capital cost threshold, and (for the hydrogen-fueled units) high fuel prices. We are slowly seeing this happen, through big changes to the supplier landscape, the IPCEI initiative in Europe, significant capacity upgrades to fuel cell production, and the Inflation Reduction Act in the US. But for now, the message remains the same: sustained support from governments is still needed to allow fuel cells to fully support the energy transition. Some fuel cell companies are now also purposing their designs to electrolysis, to help push the market, and with it the hockey stick.

ERM’s Review, a digest of the year’s activity, together with an analysis of fuel cell shipments by region, type and application year on year, is available at http://FuelCellIndustryReview.com. The 2022 edition is delayed, but coming soon. We would like to thank all the fuel cell shippers who graciously provide shipment numbers to us each year, which helps underpin our review.

Author: Stuart Jones, ERM, London, UK, Stuart.Jones@erm.com

by Lewitz | Feb 20, 2024 | Germany, News

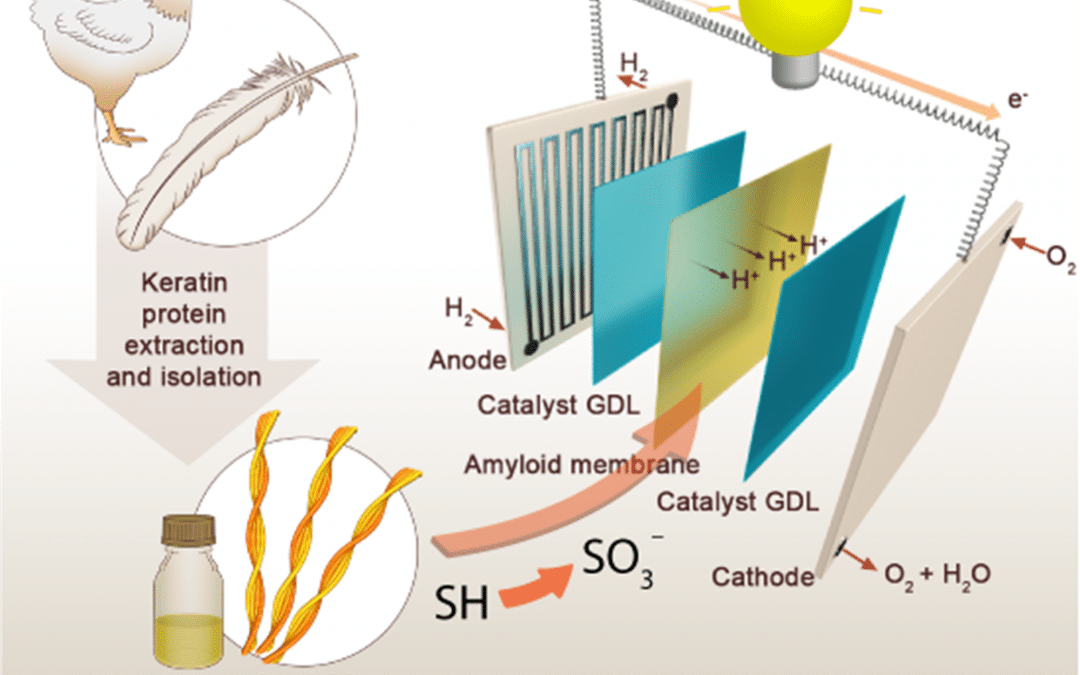

Feathers from chickens or other poultry could in the future help make fuel cells more effective and cheaper as a material for membranes. Researchers at ETH Zürich and Nanyang Technological University (NTU) in Singapore have extracted the natural protein keratin from waste feathers, which as a protein building block is an essential component of hair and therefore a natural product. Every year, 40 million metric tons of the waste accrue worldwide, which otherwise is for the most part burned. The researchers process the keratin into extremely fine fibers in order to weave membranes from them. These are then used as electrolytes in the fuel cells.

In conventional fuel cells until now, toxic chemicals have been used for such membranes. They additionally are expensive and not ecologically degradable. The new membrane, on the other hand, is much less expensive. The production in the laboratory, according to ETH Zürich, reduced the cost to one third of the conventional. The chicken feather membrane could also be useful in H2 production by electrolysis, because the membrane is proton permeable and allows the particle migration between anode and cathode necessary for water splitting.

Advertisements

As a next step, the researchers will now investigate how stable and durable the keratin membrane is. The team has already applied for a patent for the membrane and is now looking for investors or companies that want to further develop the technology and bring it to market.

Author: Niels Hendrik Petersen