The energy transition in Europe can only succeed if CO2-intensive sectors are rapidly decarbonized as well. In this, green hydrogen will very likely play a central role. Because in many energy-intensive applications, there is no other CO2-neutral alternative. The quantities of hydrogen required to achieve climate neutrality are very high for Europe, however. For decarbonization of today’s H2 production in Europe, about 250 TWh of H2 would be needed. In its hydrogen strategy, the EU assumes an availability of 2,250 TWh by 2050.

Advertisements

As the energy crisis in the previous year showed, dependence on imported energy sources is strategically risky. In this respect, larger quantities of hydrogen should be produced in Europe in order to avoid falling into comparable dependencies to that today with fossil energy sources.

In this context, as an independent technological consulting firm in Germany, DNV has investigated for gas grid operators Gascade and Fluxys the extent to which offshore hydrogen production is economically and strategically sensible and how a large-scale integration of offshore electrolysis into a European grid could make a significant contribution to the supply security of Europe.

Offshore wind energy is most economical

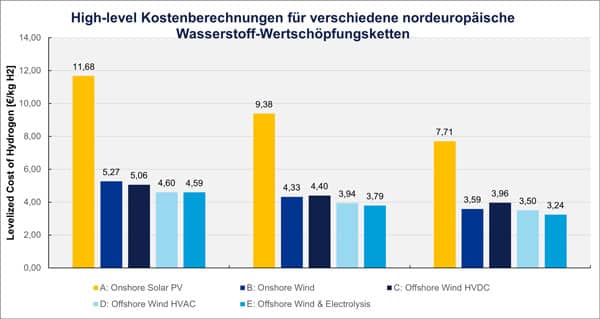

The starting point for the investigations is a comparison of five H2 value chains examined with regard to their H2 generation costs. This assumes production in Central Europe with respect to the wind and solar profiles. Compared are the production chains: onshore wind, onshore PV, offshore wind with onshore electrolysis and HVAC (high-voltage alternating current) or HVDC transmission, and offshore wind with offshore electrolysis and pipeline transmission.

The results of the modeling show that the production of hydrogen by offshore wind energy is in principal the most economical. This is particularly due to the high full load hours – about 5,000 – of the electrolyzer that offshore wind can achieve and through which the capital costs in relation to production become most advantageous.

With the use of offshore wind energy, there is still the question of whether electrolysis should rather take place onshore or offshore. This aspect as well is examined in detail in the study. A comparison of the importance of energy transmission costs on total LCOH (levelized cost of hydrogen) between the three options

1) wired HVAC connection with electrolysis onshore and

2) wired HVDC connection with electrolysis onshore versus

3) pipeline-based hydrogen transmission with electrolysis offshore

shows that up to a distance of about 125 km (78 mi) off the coast, HVAC transmission is more cost-effective compared to HVDC transmission. At distances beyond this, however, pipeline connection is more cost-effective, based on total LCOH. Electrolysis for more distant offshore areas should consequently be carried out offshore. For the study, this limit is drawn at 100 km, as a single pipeline can also integrate several offshore wind farms (see yellow-hatched area in Fig. 2).

If land use, as onshore electrolysis takes up significant area, is considered as a further factor, offshore electrolysis has yet another advantage: The already very intensive land use onshore will not be further intensified. The compact design that is possible offshore is significantly more advantageous.

89 gigawatts in the North Sea in planning

In a next step, the study investigates the offshore wind generation potential for areas in the North Sea and Baltic Sea with a distance to shore of more than 100 km (62 mi). Only those areas are taken into account that have so far been designated for wind projects by the respective countries. The corresponding evaluations show that within the 100 km criterion, 89 GWel of offshore wind energy projects in the North Sea are currently for the most part in the early planning phase. There is still far more potential in the surfaces of the North Sea; however, they are not currently designated for use for wind energy.

If the identified wind potential in the North Sea of 89 GW were to be used exclusively for the generation of hydrogen, then this would correspond to an H2 production volume of around 350 TWh per year, or 9 Mio. tonnes annually. Such a quantity would cover 15 to 20 percent of Europe’s hydrogen demand in 2050, depending on the forecast study used as a basis.

In the Baltic Sea, the potential is significantly lower, at least if the 100 km criterion is stringently applied, because of the shorter distances of the stations from the coast. A deep look at the production potential in the Baltic Sea region was not conducted in the study. However, a corresponding offshore wind backbone in the Baltic Sea could also efficiently drive an onshore H2 production in Sweden and Finland with transmission to Central Europe and additionally be combined with a production at sea.

Differences between natural gas and H2 pipelines

Basing upon the results of the economic viability and the possible potentials from the areas, the study next details the possible technical implementation. Here, it is less about the offshore electrolysis itself, but specifically about options to connect offshore hydrogen production to an onshore grid via an offshore pipeline network. For this, numerous issues need to be addressed, in order to create a hydrogen backbone that can be operated safely.

When comparing for example the transport of natural gas, which is common in offshore environments, with the transport of hydrogen, which has not yet been carried out in offshore environments, several aspects must be taken into account. First, natural gas and hydrogen have different energy contents when they are transported through a pipeline. Natural gas consists mainly of methane (CH4) and normally has an energy content – upper calorific value – between 34 and 43 MJ/m³.

Hydrogen, on the other hand, has a much lower volumetric energy content than natural gas of about 12.7 MJ/m³. This means that when hydrogen is transported through a pipeline, a much larger volume of gas is required to transport the same amount of energy in natural gas. Hydrogen, however, is also a much lighter gas than natural gas.

At normal temperature and pressure, for example, a cubic meter of hydrogen has about one-ninth the mass of a cubic meter of natural gas, which results in a much higher flow rate at the same pressure differences. The combination of these two aspects – low calorific value and light weight – has an equalizing effect, so the energy transmission of hydrogen and that of natural gas are nevertheless similar.

Furthermore, hydrogen has a much higher diffusivity in steel than natural gas and therefore promotes the embrittlement of pipelines following cyclic loadings. This effect can be controlled by an avoidance of cyclic loading, using lower quality steels, – which are softer and therefore less susceptible to cracking – and using a thicker pipeline wall. This also generally limits, however, the ability to reuse existing natural gas pipelines for hydrogen transport.

Taking all this into consideration, the study therefore comes to the conclusion that due to its different volumetric, gravimetric and molecular properties, the transport of hydrogen differs greatly from that of natural gas in offshore pipelines. Offshore hydrogen pipelines should therefore fulfill specific design criteria in order to ensure adequate transport capacity and to be able to operate safely and enduringly. On the basis of the analyses carried out, whose key points alone are treated in this article, the authors conclude that a repurposing of existing offshore pipelines is in most cases uneconomical, especially if the pipeline is to be part of an integrated system and connect several wind farms.

High pressure level possible

As a final step, the study details the technical implementation of a hydrogen backbone in the North Sea. Discussed are, among other things, questions regarding pipeline routing and pressure regimes as well as pipeline costs and required storage capacity as a result of fluctuating H2 production. The transport network sketched in the study connects wind farms in the North Sea with onshoring points in six countries bordering the Sea. For the connection, terminal points on the planned onshore backbones in the countries were selected. The network thus formed has a total length of 4,500 km (2,800 mi) and generally has a north-to-south flow direction.

In the study, a complete hydraulic analysis is not performed, but rather a few approximate calculations. In order to, for example, determine the required feed-in pressure for the transport of hydrogen from Norway to Germany, corresponding calculations were carried out for the necessary pipeline sections (see Fig. 3).

The assumed pipe diameter is 48 inches (1,200 mm). With these parameters, the required feed-in pressure was calculated for different capacities of the pipeline. For an H2 capacity of 25 GW connected to this pipeline section, for example, an inlet pressure of 192 bar is calculated. This is a very high pressure level for offshore H2 pipelines.

The DNV joint industry project (JIP) H2Pipe at this time is investigating the design, construction and operation of offshore H2 pipelines with a pressure of up to 250 bar. Although these pipelines are not commercially available yet, DNV and the JIP partner companies see no major technical constraints to the realization of such pipelines. The economic feasibility in terms of material selection for the pipelines and ancillary equipment, however, will have to be demonstrated in the coming years.

In addition to the pipeline system, the storage demand is also analyzed in the study. Connection to sufficient storage capacity is necessary for near-continuous supply over time. On this, the study shows that about 30 percent of the annual production must be stored, as a prerequisite for this H2 supply based on fluctuating renewable energies. The study accordingly assumes a connection to salt cavern storage facilities in northern Germany and the Netherlands.

Cost calculation

The costs for the outlined network were subsequently estimated. For the North Sea, the total length of the planned backbone is 4,200 km (2,600 mi). Assuming a pipe diameter of 36 to 48 inches (910 to 1,200 mm), the price thus lies between 3,000 and 4,500 euros per meter of pipeline.

According to the assumptions made, the additional LCOH for the pipeline system is between 0.13 and 0.20 EUR per kg hydrogen, i.e. 4.0 to 6.6 EUR per MWh. Since the levelized total cost of offshore hydrogen is 3 to 5 EUR per kg, this means an addition of only 2.6 to 6.7 percent, based on direct production costs.

In addition to pipelines, an appropriate compression regime must be considered. The cost of a compressor varies considerably with the size. The maximum capacity of today’s compressors is about 16 MWel (input capacity). Under the assumption of central compressors for a wind farm; an output pressure of the electrolyzers of 30 bar; an input capacity of the hydrogen backbone of 200 bar, and an arrangement of four compressors, each with 50 percent of the total capacity required and 200 percent of the installation costs; the investment amounts to 46 million EUR for a 1‑GWel wind farm and 66 million EUR for a 2‑GWel wind farm. Thus, the additional LCOH is between 0.06 and 0.08 EUR per kg hydrogen, which corresponds in value to 2.0 to 2.7 EUR per MWh. Since the levelized total cost of offshore hydrogen is 3 to 5 EUR per kg, this means an addition of 1.2 to 2.7 percent.

Overall, the cost for the pipeline and compression is around ten percent of the total specific cost of hydrogen. In addition to pipeline and compression costs, the storage must also be considered as a third component to be added to the LCOH. The result is an additional 0.22 to 0.35 EUR per kg H2 for this.

With the determined system components, the investment costs were estimated in the study as 35 to 52 billion euros to build the outlined North Sea hydrogen backbone. In conjunction with the results of the LCOH analysis, hydrogen from North Sea offshore wind farms can be supplied to Central Europe with it at specific costs of about 4.69 to 4.97 EUR per kg in year 2030. From the point of view of the authors, these costs are competitive with the cost for imports.

In order to implement the outlined system, a coordinated and swift action by the coastal nations involved is imperative. Only so can the necessary network and scaling effects be realized, and an offshore backbone contribute to hydrogen supply to Europe by 2050.

Authors: Claas Hülsen, Ton van Wingerden, Daan Geerdink

Behind us lies an extraordinary period with a plurality of crises: pandemic, war, climate catastrophe, energy scarcity, inflation, etc. Even if the acute phase of the pandemic is over, other crises are still ongoing and will presumably remain with us for some time to come.

Advertisements

Nevertheless, in the meantime, some things have settled into place. Inflation is not rising further at least, and the natural gas situation has been mastered, for the time being. Even the blackout predicted by some after the shutdown of the last three remaining nuclear power plants in Germany did not materialize. Instead, there is more renewable energy in this country than ever before – particularly in the electricity sector.

A good opportunity to take a breath and take stock of the situation: Where do we stand today? How is the energy transition progressing? What has been achieved so far in H2 and FC technology?

I have been engaged in hydrogen and fuel cells since 1997. At that time, this topic was a teeny-tiny niche. Fuel cells seemed interesting because they emit only hot air – only steam –and no harmful carbon compounds at all. There was hardly any literature on them; only a few research activities and demonstration projects. Federal support programs for them were nil.

A few car manufacturers were “already” experimenting with metal hydride storage for FC cars in the 1990s, and others with hydrogen. At the turn of the millennium, the first H2 and FC trade fairs and congresses emerged, but a portion of these disappeared again shortly after.

Optimistic developers joyfully announced back then that hydrogen-powered vehicles would be on the roads in 2004, and fuel cell-powered heaters in basements. Instead of series production, however, what followed were promises that it would finally happen in 2007, 2010, 2014 and 2017. H2 hype followed H2 hype, but of a market, there was no sign.

At times, the fuel cell had already been laid to rest – at least in the media. Several areas of application that were considered at the time lost interest. For example, the fuel cell-powered movie camera or the FC cargo bike.

New momentum first came into play in the 2010s, when hydrogen was being contemplated as a storage medium for renewable energies. Until then, it had always been said: Energy storage isn’t something we need. It was only when the idea of sector coupling emerged that it gradually became apparent that hydrogen could be a suitable medium for this purpose.

During this time, buzzwords such as power-to-gas, decarbonization and electrification emerged. The fuel cell fell little by little out of focus; however, increasingly more sights were set on hydrogen.

Nevertheless, several years passed in which the much-invoked Energiewende (energy turnaround) did not really gain ground. It took events like Fukushima, Dieselgate, debates on the health-related limits of emissions, and the founding of Fridays for Future until it became clear to political decision-makers as well that we can’t get by without hydrogen.

What then followed was the European Green Deal and numerous national hydrogen strategies in many countries around the world. The first large commercial and industrial businesses began to change their strategy and – at least partially – turned away from fossil energy structures.

It became increasingly clear that solar and wind power, – contrary to the many prior negative prognostications – together with suitable energy storage, have the potential to defossilize not only the power sector but also other energy sectors.

Most recently since the Russian war of aggression on Ukraine, it has become obvious that the times of cheap fossil energies are over, once and for all – which is positive in multiple respects. Because high prices for natural gas, oil and coal, which are likely to keep rising due to the growing cost of CO2 certificates, not only reduce energy consumption, they demand a change to more decentralization as well as more independence.

But where do we stand now?

Today, we have available to us almost too many H2 trade fairs and congresses – worldwide. We have investment commitments in the billions from major corporations. We have political strategies for establishing a Europe-wide H2 backbone in order to distribute renewable energies in the form of H2 gas across the continent.

We also have, however, millions of citizens who are very unsure and fearful of the future. Many cannot afford either heat pumps or electric cars. So their complaints are loud but, at the same time, understandable. That is why it is all the more important today to explain the energy transition, as well as H2 and FC technology, in a way that makes sense.

We are at the beginning of a gigantic transformation process that demands a lot from us all. At the same time, this process holds immense potential for development and redevelopment. That’s why it’s crucial to talk more about opportunities and less about problems.

I am absolutely certain that this process of change is possible without substantial loss of prosperity. We can show how new jobs can be created, how sustainable environmental standards can be set, how resources can be conserved, and at the same time how the standard of living can at least be maintained, if not improved– worldwide even.

A prerequisite for this, though, is that we do not leave everything up to the free market, but rather create suitable framework conditions that offer sufficient freedom to act but also planning security and, above all, are generation-fair.

At this year’s H2POLAND exhibition in the Polish city of Poznań, representatives of the “three seas states” took part in a signing ceremony to formally launch a joint hydrogen project. The countries involved in the initiative are all European Union members located between the Baltic, Adriatic and Black seas, namely the Baltic states, Poland, Ukraine, Hungary, Czech Republic and Slovakia.

Advertisements

Tomoho Umeda, founder of Polish companies Hynfra and Hynfra Energy Storage, led the discussions between the country representatives on the joint enterprise. The Polish businessman, who has Japanese roots, expressed regret that Central and Eastern Europe, or CEE for short, is rarely involved in the rapid development of the hydrogen industry in the European Union: “There’s a lot of nodding but when it comes down to business, CEE tends to be sidelined in key developments.” The three seas hydrogen project intends to change precisely that.

Shared connections

Poland is at the heart of current growth in the Eastern European hydrogen sector. That’s not just because Poland, with its population of almost 40 million people, is by far the biggest economy in Eastern Europe, but due to the large number of underground salt caverns that make it an ideal location for storing hydrogen. A fact that Umeda emphasized several times in his speech.

The countries that want to push forward the development of hydrogen industries in this region have more in common than being overlooked members of the EU. What unites them most is that they are all countries of the former Eastern bloc. This common past means they share certain similarities, as particularly evidenced by their infrastructure and the special regulation of the energy sector.

Umeda highlighted the pipeline infrastructure and heat supply in Central and Eastern Europe. Aside from a dense district heating network, common elements across these countries also include long-distance interregional connections which stem from Soviet times. New networks are also being added, such as the Lithuania-Poland and Poland-Slovakia gas connections which only became operational a few years ago.

Czech representative Vaclav Bystriansky made it clear in his address that these transmission lines as well as zero-emission energy generation have a vital role to play in the development of the hydrogen sector. In his opinion, the old model of east-west transmission is outdated and should be relinquished. He is convinced that there will be more north-south connections in future.

For his country this means working much more closely with its northern neighbors. “Poland has the storage capacity and Czech Republic has the nuclear power plants,” said Bystriansky, summarizing the direction of future cooperation.

Slovakia echoed Bystriansky’s remarks, but adding that the nations of Central and Eastern Europe have a lot they could learn from each other. This was said to include, above all else, learning from the mistakes of others. An essential point that was also stressed by other officials is the potential use of waste incineration for the production of hydrogen. Incineration is currently a weighty issue in Eastern Europe. The view from the Slovakian side: “You shouldn’t just get fixated on renewables alone but instead use what makes sense and satisfies the conditions.”

Estonian delegate Sven Parkel responded that countries in Central and Eastern Europe could only earn a better position in EU committees by joining forces. He said they must represent their interests in Brussels collectively, otherwise they would not be heard by dominant EU countries such as Germany and France. What’s more, Parkel suggested that they should put on a united front when addressing the regulatory elements of the region’s hydrogen industry at an administrative and public authority level.

Ukraine boasts greatest hydrogen potential

István Lepsényi from the Hungarian Hydrogen Technology Association, who took his place right next to the Ukrainian delegate Oleksandr Riepkin, astonished the gathering in Poznań with his particularly political statement. In contrast to the pro-Russian position of Hungarian Prime Minister Viktor Orbán, Lepsényi expressed his personal feelings in relation to Ukraine’s struggle against its Russian aggressor. He hopes Ukraine will soon win and an end will be brought to a horrendous war which the Russians have waged against Ukraine.

Ukraine and its hydrogen potential was one of the thematic high points of the panel discussion which preceded the signing of the joint hydrogen project. Oleksandr Riepkin started by thanking first of all Poland for preventing the certain death of millions of people from Ukraine by opening its hearts and homes and offering all it has to the Ukrainians fleeing the rape and murder of the Russians. The audience responded with almost unceasing applause and cries of solidarity. He also announced that his country would be entering a hydrogen partnership with Poland, saying: “As sisters and brothers, Poland and Ukraine can achieve anything and be a match for anyone.”

After Riepkin had detailed Ukraine’s options for zero-emission electricity generation, he turned his attention to the existing collaboration with Poland on energy issues. The power connection between the countries has now been reestablished and in future could be extended and utilized for hydrogen production. The Ukrainian suggested that CEE nations should specialize in individual areas, thus sharing the load which would be important for competitiveness in the hydrogen industry.

“Central and Eastern Europe should also step out from under the shadow of Western Europe and itself manufacture the electrolyzer plants that enable hydrogen production. A domination of Western European technology is to be avoided,” the audience in Poznań was told. “Our technology is just as good as German technology – only more affordable,” added Czech delegate Bystriansky.

Riepkin then took a look at the problems that could ensue from hydrogen production in the CEE region. For instance, there are now drought-prone areas where conflicts could arise with agriculture in relation to water supply and land for renewable energy. Producing hydrogen using nuclear power could be an alternative, as expressed by the Czech and Slovakian representatives.

The three seas hydrogen project appeared ready to expand toward Scandinavia, with Estonia and Finland being obvious candidates. Both countries have connected up their gas pipelines in a move that creates promising opportunities for hydrogen grids. There was likewise optimism that the two remaining three seas states – Romania and Bulgaria – will join the hydrogen initiative in the foreseeable future.

The decline in the share price of Ballard Power in the past months is ascribed to the impatience of the many investors who assess primarily the short-term potential of this market leader in the PEM FC area. What counts is the long-term outlook of the company.

Current quarterly figures give credit to the skeptics. Ballard itself is not fighting this, as they are working unperturbed on the long-term strategy: establish production capacities, cooperations and pilot projects. This will be accompanied by capital outflows as well as the “logical” losses that it will entail. Ballard has enough capital in the bank to be able to implement the plans without outside pressure: 864 million USD in the bank account speaks for itself.

Advertisements

At the same time, Ballard is working on the constant optimization of its technologies, be it the MEA for the fuel cell, the FC modules, or the stacks for various applications, to be among the top suppliers on the market. But how will the stock market react when the production sites in China, Europe, the USA and Canada (eventually also in India – see Cummins with Tata) are utilized to capacity and then promise, in addition to high sales growth, a good profit?

China could be the wild card

Ballard president Randy McEwen is traveling for several weeks through China to meet with representatives of public authorities, ministries, companies, customers and municipalities as well as other players important for Ballard. This is certainly about understanding why China’s H2 support program has yet to be approved. The probably still largest FC stack production facility in the country – operated as a JV by Weichai and Ballard – is still “unemployed.”

That a larger program will come is, for me, no question, as many companies and regions or cities in China have now seized the topic in a variety of ways on their own (e.g. capacities for different electrolyzer types, stacks, vendor parts, FC trucks, H2 pipelines, refueling stations). For these is expected a high growth potential, which ought to be made use of. Perhaps China will still surprise the world with an H2 program in 2023 that not only matches, but makes the equivalent programs in the USA, Europe, Japan and elsewhere look smaller?

What would happen if China also gave passenger car fuel cells a boost with a national quota? China already did this for the battery– in the largest automotive market in the world – with the EV mandate, and all auto companies producing in the country have had to adapt to it. Ultimately, China has provided the foundations for battery-electric mobility worldwide.

By the year 2030, 1 million vehicles refuelable with hydrogen are to be running in China. Perhaps this goal will be adjusted against the South Koreans, since South Korea wants to be able to fuel over 6 million vehicles with hydrogen by 2040. For Ballard, a positive turnaround could come about very quickly from this, which would then also help the share price soar.

150 million kilometers clocked

Ballard meanwhile reports 150 million kilometers driven (93.2 million miles) by commercial vehicles and buses equipped with its technology – and smoothly. Worldwide, 3,800 buses are driving with Ballard inside. The Canadian company is setting an industry and sector standard with this. They are very well positioned in terms of total cost of ownership, according to CEO Randy McEwen.

“At Ballard, we are designing our PEM fuel cell engines for heavy-duty mobility applications where zero emissions, reliability, and durability are key differentiators for end-user total cost of ownership. We continue to set the industry benchmark for PEM fuel cell performance in our target markets. The accumulated distance driven by FCEVs powered by our technology underlines Ballard’s customer focus and commitment to reliable service and high uptime. We achieve this industry milestone at a time when we are seeing growing customer interest in the adoption of hydrogen fuel cells in our key mobility verticals of bus, truck, rail, and marine, as well as off-highway and stationary power applications.”

Randy McEwen, Ballard chief

First quarter has little predictive power

Order volume ended up good: 137.7 million USD, a doubling from the same period the previous year. Turnover for the quarter reached 13.3 million USD, which was below analysts’ expectations. Good things can be expected from the second half of the year. McEwen sees a very busy second half of 2023 and an excellent year 2024.

In the bus sector came three new OEMs, so companies that build buses and are relying on the FC module and knowhow from Ballard. Van Hool and Solaris have long been satisfied customers. Over 500 FC buses are currently set to be ordered in Europe, a large share of which equipped with Ballard. Meanwhile, 1,500 transit buses are in the tendering process – in Europe. For me, however, this is just an indicator of a development that will really pick up speed in the coming years.

The same pertains to commercial vehicles, where gradually the major truck manufacturers are turning, in addition to battery-electric solutions, to hydrogen. About this, McEwen said, “To be clear, the truck market is in the very early phases of fuel cell market adoption.” Here, Ballard is supplying stacks to various OEMs such as Quantron, and further customers may follow. In the area of trains, things are also slowly getting underway, which the rising orders of Ballard partners Stadler and Siemens Mobility show. Their customers are increasingly opting for a mix of battery-electric and hydrogen-powered trains. Ballard is also well positioned here – often in competition with Cummins or Alstom.

First Mode has raised its order for FC modules for heavy mining trucks from 30 to 35, and it’ll be likely 400 units in total for its partner Anglo American. For Canadian Pacific Rail (CP), locomotives have already been equipped with FC modules. Larger orders will probably come, and can be expected in the second half of the year.

In Norway, meanwhile, the ship MF Hydra was put into operation. Liquid hydrogen is turned into energy with the help of Ballard’s 200-kW module. The ferry for 300 people can travel for up to 21 days with it.

Everything out of pocket

The capital invest in the amount of 37.5 million USD in the first quarter mainly went into increased spending on R&D and product development – with over 860 million USD in the bank, not an issue. Interesting is an analyst’s question of why Ballard wants to allow new authorized capital to be given (so the possibility of issuing further shares), since it has sufficient liquidity at its disposal. This here is only about an extension of an expiring program or entitlement to issue further shares, so the tenor. They will also not make this a custom, was the answer.

I would interpret it differently: Ballard could quickly issue further shares if a takeover (acquisition) of a strategically interesting company presents itself, and quickly generate own capital through these shares or their equivalent, without having to dig into the high cash cushion. Everything has two sides.

Summary

Ballard may seem boring and is a big disappointment in terms of share price. The company has a very good standing, however, and is establishing and expanding its international presence, and is positioning itself so that it can in the future make and sell large numbers of stacks and modules for a variety of FC markets and thus earn money. As a partner of various OEMs, Ballard can Provide FC expertise and knowhow to a number of companies. These OEMs do not need to research and develop in this direction themselves: They buy turnkey products from Ballard and enter in competition with companies such as Toyota and leading truck manufacturers.

The China card would open up all possibilities should the country agree to a comprehensive H2 program, as Ballard would then be a big winner. Besides China, Ballard should also put its focus into India, which has a strong interest in hydrogen (see report on p. 58). Ballard equipped the first H2 train to run there. Thinking about the JV of Cummins and Tata Motors, Ballard could enter a similar venture with Ashok Leyland or Reliance. But that is only my personal view. Whoever sees Ballard in the medium or long term should use the severely depressed share prices for new and further buys.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

A strong transport network is a prerequisite for a future H2 economy. “Only so can the hydrogen quantities be transported that our industry requires,” also knows Prof. Jörg Steinbach, the economy minister for the German state of Brandenburg. He presented a feasibility study in February 2023 containing concrete routing networks to be established for various time periods. “The identified possibilities for drawing on existing natural gas infrastructure and bundling lines (to also transport hydrogen) indicate that we can save about 55 percent of the investment costs needed to build a completely new pipe network,” according to Steinbach.

As part of the study conducted on behalf of the ministry, an analysis was provided that can be used to forecast future H2 consumption and generation potential up to the year 2045. Based on the needs identified this way, cost-efficient routing options were derived. The goal was to develop a high-level H2 transport network that connects regional producers, storage facilities and end consumers – and later integrable into a countrywide H2 infrastructure.

Advertisements

“It has a total length of about 1,100 km (684 mi),” summarized Florian Temmler, project manager at Infracon Infrastruktur Service. Of this, about 600 km will consist of converted natural gas pipelines and about 500 km, of new lines. “By this, an economical construction of the network in Brandenburg is guaranteed.”

“It has a total length of about 1,100 km (684 mi),” summarized Florian Temmler, project manager at Infracon Infrastruktur Service. Of this, about 600 km will consist of converted natural gas pipelines and about 500 km, of new lines. “By this, an economical construction of the network in Brandenburg is guaranteed.”

The study also shows for the first time the scope of the required investment: 1.221 billion euros. It was prepared by a consortium made up of Fraunhofer IEG (energy and geothermal research), Fraunhofer ISI (systems research), the Reiner Lemoine Institut (RLI) and INFRACON Infrastruktur Service.

The online hydrogen marketplace for the region launched in 2022 (Wasserstoffmarktplatz Berlin-Brandenburg), according to Steinbach, is already enabling a picture of how great the demand is: Nearly 300 businesses and institutions with over 300 projects are already registered there. That’s because Brandenburg is, on the one hand, a significant area for energy imports and exports. On the other hand, it has considerable potential for green electricity and hydrogen generation as well as their utilization.

“In the long term, regional hydrogen production could rise to over 20 TWh, with especially high potential from former coal mining stations,” says Thorsten Spillmann from Fraunhofer IEG. Eventually, it could even become 40 TWh, with more than two-thirds coming from industry.

At the moment a fierce debate is raging over whether the current operators of natural gas networks should also be the ones to manage the hydrogen grids of the future. European Union-wide regulations on unbundling require the separation of network operator activities. According to Germany’s Federal Network Agency, “transparency and the non-discriminatory configuration of grid operations are fundamental prerequisites to promote competition in upstream and downstream areas of the value chain and to create trust among market participants,” which is why unbundling is said to be essential. So far this provision has only affected the electricity and natural gas networks. But now that there are plans for a pan-European hydrogen grid, a question mark hangs over which rules will apply to it.

The European Commission wants to standardize the rules at a European level and hence is revising the EU directive and regulation concerning the internal gas market. The previous draft states that in future distribution system operators would have to sell off their hydrogen grids, leaving them, at most, with a minimum stake and limited voting rights. This divestment would be obligatory if the energy supply company were already operating a gas or power network. As such, this would result in nearly all transmission system operators in Germany being forced to disincorporate their hydrogen operations. Since the proposals would not provide an incentive to convert existing gas networks to hydrogen, this creates a conflict with current policy targets and the aims of Germany’s national hydrogen strategy.

Advertisements

The reason why the EU still favors this route is because it assumes different framework conditions than the ones that prevail, for instance, at a national level, e.g., in Germany. Thus the EU makes no distinction in its draft legislation between transmission system operators and distribution system operators. The particularities of German law are therefore not taken into consideration. In addition, the EU doesn’t focus on the widespread conversion of existing natural gas grid infrastructure, but instead places the emphasis on the production of climate-neutral gases that are expected to be injected into the current natural gas network. The operation of hydrogen-only grids is viewed more as an add-on to the existing methane grid, while Germany sees hydrogen-only grids as the default option.

Ehler welcomes new legislation

On Feb. 9, 2023, the European Parliament’s Committee on Industry, Research and Energy voted on legislative proposals for its gas market and hydrogen package. CDU Brandenburg politician and MEP Christian Ehler, who is also industry and energy policy spokesman for the EPP Group in the European Parliament, explains further:

“In order to meet EU climate targets and decarbonize our manufacturing industry, our energy system has to be completely restructured. The gas market and hydrogen package is a crucial piece in the jigsaw for the overall “Fit for 55” legislation and the EU instrument for decarbonization in the gas sector. For industry especially, this will only happen with hydrogen and its associated infrastructure.

It is now extremely important to stimulate the hydrogen market by speeding up the arrangements for hydrogen production, making it less bureaucratic and urgently developing a plan to create a European Hydrogen Backbone (EHB). The European Hydrogen Backbone offers the opportunity to revitalize the European industrial economy while at the same time ensuring the resiliency of the energy system, fostering greater energy self-sufficiency and maintaining security of supply throughout the whole of Europe.

Thanks to today’s ballots, our committee has now laid the key foundations. A great many items in the two dossiers voted upon contain a clear improvement with respect to the commission’s proposal. That applies particularly to the unbundling rules in the directive. All unbundling models that we are familiar with from today’s gas and electricity market are to be made available for an unlimited time. This will create incentives for the repurposing of existing pipelines as hydrogen pipelines since the network operators will benefit from their investment in hydrogen infrastructure.

According to the commission’s proposal, they would have to sell their hydrogen infrastructure in 2030, which would inevitably prevent them from investing in hydrogen infrastructure, and would have negative consequences for the development of a hydrogen backbone.

Hydrogen offers huge opportunities for Brandenburg; it is an attractive location for an electrolyzer industry. The energy transition can only succeed by involving gaseous energy carriers. Regrettably, many of the pathways set out in the proposals of the EU Commission are being held back by individual rules. This is because the proposals make the false assumption that industry’s gas demand can be managed by concentrating on the transmission system without recourse to brown coal.

In actuality, most commercial customers in Germany purchase gas via these distribution systems. The EU Commission’s approach therefore needed a correction. Gas distribution systems must not be excluded from conveying hydrogen in the future. The whole of Brandenburg should put itself forward as a model region for energy. Here, hydrogen will serve as a medium for storage and transportation – in addition to its use as a fuel. The aim is to connect the industrial and production sites for green hydrogen in the Mark Brandenburg area to the future European hydrogen grid.

Today we have set out how renewable and low-carbon gases can be more easily injected into the existing gas grid and how it should be possible to establish a dedicated hydrogen infrastructure and its own hydrogen market. The hydrogen grid of the future will evolve from the gas grid of today. The framework conditions agreed today will help to ensure the hydrogen grid is set up at the required speed and with the required expertise.”

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.