by Monika Roessiger | Apr 16, 2024 | Energy storage, Fuel cells, Germany, hydrogen development, international, News

Optimism at the H2 Forum in Berlin

A good 450 participants gathered at the specialist conference H2 Forum in Berlin February 19 and 20 to discuss innovative H2 technologies, strategies for the market ramp-up and the necessary regulatory framework conditions. A further 1,000 participants were connected online, even despite the considerable time difference in countries such as India and the USA.

The event was opened via a video by Kadri Simson, EU Commissioner for Energy. The two-day program was held under the motto “Empowering the future of hydrogen,” where this year’s focus was on the production of the green gas by electrolysis and its transport in Germany and Europe. At the H2 Forum were, among others, representatives from E.on, Enapter, EWE, Linde, FNB Gas and the H2Global Foundation. They discussed the role of hydrogen in the defossilization of the economic systems. Philipp Steinberg of the German economy ministry outlined the various phases of the development of the hydrogen core grid in Germany.

Advertisements

Feelings of optimism and assurance were tangible throughout the high-ceilinged rooms of the Estrel Congress Center (ECC) as players from politics, industry and the energy sector talked about ambitious H2 projects at home and abroad. Inspiring as well was the approval by the EU Commission a few days before of a series of IPCEI projects, thus ending for some participating companies years of waiting. Additionally, the carbon contracts for difference and the auctions of the European Hydrogen Bank are giving hope to business representatives.

Spain: Megawatt-electrolysis in practice

For example, Özlem Tosun, project manager for green hydrogen at Iberdrola Deutschland, reported on the experience with a 20‑MW electrolysis plant, making it currently the largest in Europe. “I hope it doesn’t stay that way,” she added, in view of the necessary market ramp-up for green hydrogen. The Spanish energy corporation, known in the country primarily as an operator of wind farms in the Baltic Sea, started operation of the plant in Puertollano, May 2022 in the presence of the King of Spain. The city with nearly 50,000 inhabitants is located about 250 kilometers south of Madrid. The electricity for the hydrogen production comes from a 100‑MW photovoltaic park a few kilometers away and flows via an underground cable into the production hall, in which 16 electrolyzers of 1.25 MW each perform their work. These produce annually up to 3,000 tonnes of green hydrogen, which is temporarily stored in tower-high pressure tanks at 60 bar. The electrolysis plant is located next to the fertilizer factory of Fertiberia and currently covers ten percent of their hydrogen requirement, which according to Iberdrola saves 48,000 metric tons of CO2.

“But this is just the beginning,” stressed Tosun. “In the coming years, Iberdrola wants to increase the production more than tenfold – to 40,000 tonnes by 2027.” The demand is there, since otherwise Fertiberia is using for its ammonia synthesis gray hydrogen obtained from natural gas. That no comparable plant for the production of green hydrogen on an industrial scale is yet in operation is also due to the fact that the whole thing is not as simple as it sounds in the big plans and letters of intent. “It didn’t go smoothly from the start,” admitted Özlem Tosun. “On the contrary – we had a lot of problems. But we also learned a lot and were able to improve a lot as a result. Not only technically, but also economically.” One of the most important points was to optimize the efficiency of electricity use. Contributing to this was that the performance and efficiency of the electrolyzers were able to be increased further and further.

Overall, the practical experience in Puertollano was important “to be able to scale the system.” As far as the large-scale production of climate-neutral energy sources is concerned, the multinational energy company not only sees itself as a pioneer, but is also optimistic about the future. Because Spain first wants to become independent of fossil fuel imports and then be able to export renewable energies. So it’s no wonder that Germany is for Iberdrola “a key market,” as Tosun says, “especially for green hydrogen.”

Lack of regulation as a stumbling block

How the development of a German and European hydrogen industry can be accelerated was one of many other topics discussed at the conference. It is important to break down barriers – for example lack of regulation and infrastructure – it was said in a panel discussion. Such hurdles, the speakers agreed, were in addition to the high costs for H2 production, like before, the crucial reasons why not a small number of companies, despite the positive feasibility studies, are still waiting with the final investment decision. The following figures show just how wide the gap is between aspiration and reality when it comes to the gas of the future: In recent years, the German government has raised the target for domestic production of green hydrogen from the original three gigawatts to ten gigawatts, yet so far not more than 62 MW of generation capacity has been installed. That there is a long way to go, but which can go faster, further practical examples have shown.

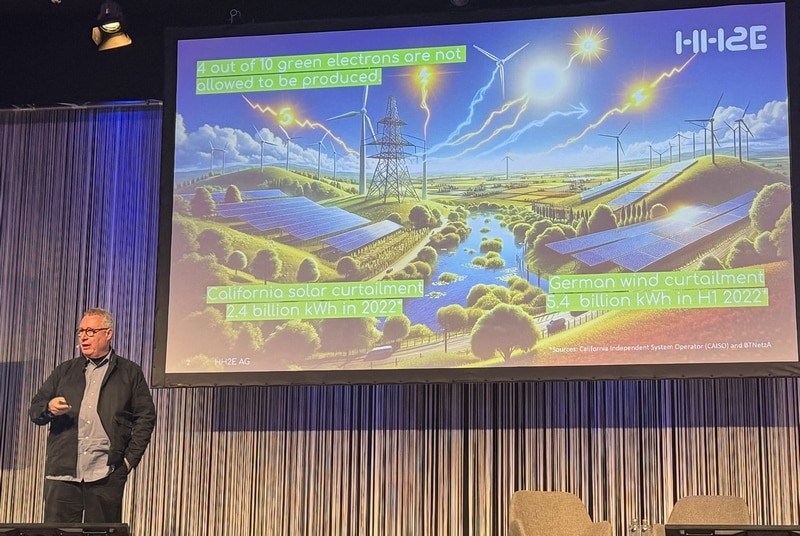

“Never waste a green electron again!”

“Did you know that with the wind power that was curtailed in the first half of 2022 alone 1.5 million households in Europe could have been supplied with electricity for a year?“ (The figure refers to average households with a consumption of 3,500 kWh per year.) That was one of several questions with which Alexander Voigt, managing director of HH2E, began his speech. “What could we do with all the green electrons that are not being generated only because the power grid cannot absorb them?” His answer, of course: Hydrogen! But also high-performance battery storage, to be able to offer energy for stabilization of the power grid. That’s how he explained the business model of the planned HH2E factory in Lubmin, Germany. It will use surplus electricity to “reliably and cost-effectively produce green hydrogen.” In addition will come CO2-free heating and, if required, the conversion of the “green molecules” back into electricity.

Alexander Voigt, CEO von HH2E, nutzt künftig Überschussstrom in Lubmin (Foto: Monika Rößiger), Source: Monika Rößiger

With this, the plant could contribute to the decarbonization of industry in Germany and, at the same time, support the energy supply. The final investment decision will be made shortly, according to Voigt, and then the way would be clear for the start of construction. In the year 2026, according to the plan, energy generation is to start: around 100 megawatts of total capacity in the first expansion stage, divided between a 56‑MW electrolyzer and a 40‑MW battery storage system. The electricity for electrolysis is coming from offshore wind farms in the Baltic Sea. Initially, the operators expect to produce around 7,200 tonnes of green hydrogen per year. The production capacity of the plant is scalable up to one gigawatt. Lubmin, once a transshipment point for Russian natural gas, will then become a center for green hydrogen. This can be fed into the existing natural gas grid that extends from the northeast of Germany to the southwest near Stuttgart.

In total, more than 40 companies from the entire H2 value chain presented their solutions and products in the high glass hall next to the conference hall in the Estrel Congress Center. The organizational framework of the H2 Forum was right: There was time to connect during the coffee breaks, lunch and supper. Lively discussions took place at all the tables and stands. That more politicians were present this time than at previous events was, according to Laura Pawlik, Sales Manager of the organizer IPM, particularly emphasized in the feedback from the participants. And also that the representatives from politics and administration were definitely open to further funding.

The date for the next conference has already been set: March 4 and 5, 2025, again in the ECC in Berlin. Focal points will be in addition to politics also the regulatory progress in Germany and Europe.

by Sven Jösting | Apr 15, 2024 | Energy storage, Fuel cells, international, News, Stock market, worldwide

The share of Cummins Engine brings joy: The share price rose to a new high for the year, after the company was able to settle a long-standing legal dispute – it was about non-compliance with emission standards for engines – with a penalty payment of 1.6 billion USD, and with that this chapter is closed. The total cost of this settlement was 2.04 billion USD. Regarding the value per share, Cummins earned a good 19 USD in year 2023, if including the abovementioned costs. So it was about 6 USD per share.

The dividend remains at a high level – recently 1.68 USD per share in the quarter. Turnover increased by ten percent to 34.1 billion USD in year 2023 and should also further grow in the future. The subsidiary Accelera, which concentrates on the clean energy business (engines, batteries, fuel cells, electrolysis, etc.), was able to increase turnover to 354 million USD and should in the current fiscal year bump this up to 450 to 500 million USD. This area belongs, via the program Destination Zero, to one of the company’s future fields of focus and requires considerable investment. This division will therefore report a loss this year of 400 million USD, which, however, has its logical basis in the high initial investments. Even so, Accelera alone was already able to build up an order volume for electrolyzers of 500 million USD. The spin-off of the subsidiary Atmus Filtration Technologies to the shareholders (swap offer) is also about to be finalized. Cummins holds over 80 percent in this. The company will be valuated with 1.9 billion USD.

Advertisements

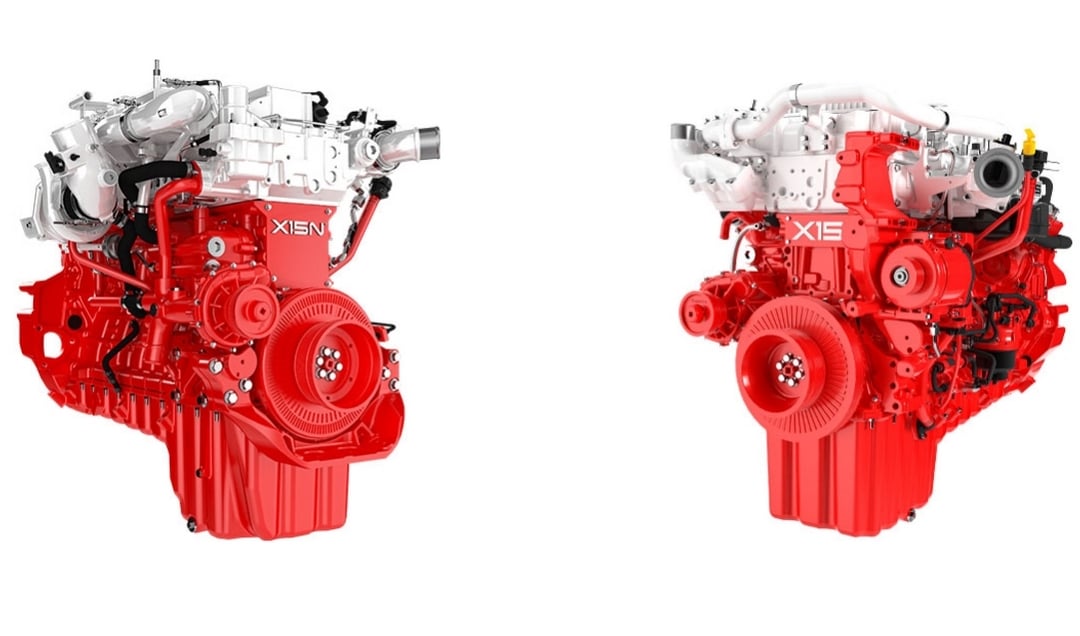

New engine development HELMTM

A share price driver, however, can be the development of a new generation of engines. These units, based on the X15 engine platform, can be operated with natural gas as well as with hydrogen (starting 2028) and e-fuels. HELMTM stands for high efficiency, low emission, multiple fuels. They should accordingly contribute to significantly reducing the diesel demand of today’s customers. Test runs are underway with Walmart and UPS, and also with Paccar for its US class 8 truck Kenworth T680. Cummins is investing 1 billion USD in this project for the time being.

At the current price level – the company has a market capitalization of about 39 billion USD – the current valuation seems sufficient to me, where Cummins is considered a standard stock with a high dividend yield. I would now remember and rather bet on the comparable competitor from China, Weichai Power, as this company is only half as highly valued as Cummins and additionally owns a special potential in the area of hydrogen and fuel cells. Cummins but will go its own way in hydrogen. The subsidiary responsible for this, Accelera, has very high growth potential, which will have a positive impact on the company as a whole in a few years’ time.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: Sven Jösting, written March 15th, 2024

by Sven Jösting | Apr 15, 2024 | Europe, hydrogen development, Stock market, worldwide

Sven Jösting’s stock analysis

#Shares from the crypto universe and from many technology companies are currently reaching new highs. Armaments are also booming on the stock market in view of the many global, some war-like, political conflicts. Only the topic of hydrogen and fuel cells is still leading a shadowy existence, with prices at crash level, which however – still – fully obscures the prospects of sustainably produced energy, and above all of hydrogen.

The stock exchange also always works according to the principle of group rotation, according to which always exactly these topics slide back into the focus and center of investor interest that have been completely neglected up to now but have excellent prospects. Precisely why I expect that, after almost three years of falling share prices, the trend will now gradually reverse and a sustainable, long-term upward trend on the stock market is beginning that is based on very high company growth.

Advertisements

To many market participants, it is unclear at this time how hydrogen will be available in large quantities, although it is already clear today that production volumes will increase enormously and prices will fall. All this, however, doesn’t happen overnight: Gigantic capacities in electrolyzer technology – PEM, AFC, AEM, SOFC – must arise to be able to produce sufficient hydrogen.

Hydrogen economy is on its way and will come!

“The H2 economy is on its way and will come,” was the conclusion of the H2-Forum in Berlin (Feb. 19 and 20, 2024, see p. 20). One speaker explained that we’ve now come, after overinflated expectations, “out of the valley of the dead” and on solid ground. Now, it’s all about assessing risks and partaking in concrete projects, which would mean investments in the whole area of hydrogen. From talk to action.

If we take a visionary look into the years 2030, 2035 and 2040, it’s clear what technologically needs to be on course today. Green and, temporarily, blue hydrogen (produced by natural gas reforming – 70 percent less CO2) will dominate and replace gray hydrogen from natural gas, eventually CO2-freely. Regeneratively produced hydrogen will be a raw material that receives a market price as a commodity on the stock exchange. Those producers who have large quantities of low-cost renewable energy (solar, wind and hydropower) at their disposal and have the necessary access to water (above all seawater) will get a tradable commodity that they can sell on the world market, with high profit margins, or use themselves.

In the last case, it can be observed that countries with ideal framework conditions are increasingly thinking about using the hydrogen produced locally themselves, by setting up corresponding industries, instead of selling it to countries like Germany, as energy is a very important location factor.

Hydrogen and the stock market

In countries such as China and individual regions like the US state of California are developing hydrogen strategies that have model character and can serve as a blueprint for the world. In China, over 1,200 H2 refueling stations are to be in operation by 2025. Currently, it’s about 400. South Korea wants long-term to establish more than 1,600 H2 refueling stations in the country. Here in Germany are, as before, around 100 in operation.

Companies with capacities for fuel cell stacks and modules for commercial vehicles are in the starting blocks (Bosch, Cummins, Ballard, Hyzon, Toyota, Hyundai, etc.), because these markets will be huge. Several million trucks and buses can be assumed to be converted to battery or fuel cell (also in combination) in the next ten to twenty years. Hydrogen engines are also attracting a lot of attention, as various prototypes have already been developed (Bosch, Cummins, Toyota).

The question of the right H2 shares can be answered well with this context, as primarily companies will win that have a mature technology, operate with robust business models, are able to deliver and possibly profit from the consumable hydrogen itself, if they can produce it themselves at low cost or distribute and use it as a commodity.

Here beckons the prospect of a good profit margin with high growth potential. On the stock exchange, however, there is right now in the area of hydrogen a phase of disappointment, as firstly everything is not going so quickly and secondly setbacks must also be overcome. In addition to questions of implementation speed, there are often also regulatory issues on the timeline. That the stock market has not yet recognized the potential of the companies through their share prices and valuations is easy to see from the current prices. There is no question that there will be a complete reassessment, however, even if it will take longer. Be patient. We are only at the beginning of this new mega-trend – also on the stock exchange. Let’s wait for the group rotation; then, everything will happen very quickly.

Disclaimer

Each investor must always be aware of their own risk when investing in shares and should consider a sensible risk diversification. The FC companies and shares mentioned here are small and mid cap, i.e. they are not standard stocks and their volatility is also much higher. This report is not meant to be viewed as purchase recommendations, and the author holds no liability for your actions. All information is based on publicly available sources and, as far as assessment is concerned, represents exclusively the personal opinion of the author, who focuses on medium- and long-term valuation and not on short-term profit. The author may be in possession of the shares presented here.

Author: Sven Jösting, written March 15th, 2024

by Hydrogeit | Apr 15, 2024 | Energy storage, Germany, Policy, worldwide

Background to the Bonhoff/BMDV split

Things had quietened down on the Bonhoff front. But then new information surfaced in February 2024 which prompted German transportation minister Volker Wissing to take action. On Feb. 15, he released Klaus Bonhoff, head of the policy issues department, from his duties with immediate effect and also moved a divisional head. The reason behind the decision lies in a discrepancy uncovered during an internal review undertaken by the transportation ministry, also known as the BMDV. The affair gained added force when German news magazine Der Spiegel reported on Feb. 20 that Wissing had stopped “completely the approval of hydrogen funding.” Yet in reality funding is not being axed. The ministry is merely carrying out reassessments that could lead to a delay.

Advertisements

But one thing at a time. In this article we’ll attempt to shed light on who did what to whom as well as how and when it all happened.

It started back in summer 2023 when German business paper Handelsblatt published an article about a questionable friends and lobbying network. The suspicion of nepotism that was raised on various sides was based on the alleged existence of an overly cozy network of contacts linking a number of different political and industry figures. Bonhoff was reproached for his reported friendship with Werner Diwald, chairman of the German hydrogen association, and its president, Oliver Weinmann, both of whom he allegedly joined on a ski trip. What’s more, it was claimed that Bonhoff helped the German hydrogen association, abbreviated to DWV, to gain funding in 2021.

Stefan Schnorr, state secretary at the German transportation ministry, was tasked with clarifying the facts and, according to Der Spiegel, gave the all-clear a few weeks later, stating there was “No trace of favoritism.” At the same time, Bonhoff received broad support, particularly from the hydrogen sector.

Everything bubbled up again in early 2024 when Der Spiegel quoted parts of an email exchange between Bonhoff and Diwald (see freedom of information website www.fragdenstaat.de). This apparently substantiated a high degree of closeness and familiarity between the two men.

Inconsistencies and contradictions

In fact, what the disclosed emails show is that certain wishes and views regarding funding measures had been articulated on the part of the DWV. For example, Werner Diwald wrote in September 2021: “In view of the upcoming elections it would certainly be good for grant approval to be given before the end of this legislative period.” (Der Spiegel, Feb. 6, 2024)

This prompted Bonhoff to forward the email to the appropriate specialist department at the transportation ministry where he inquired after the state of affairs, according to the statement he gave to H2-international. As Der Spiegel and Tagesspiegel Background, another German publication, both reported, he also “orally supported” the project. However, given this expression of support was previously denied, this admission could now cause no end of trouble for the ministry.

LobbyControl then took it as proof that favoritism was indeed at play. On Feb. 16, 2024, the online platform stated that days before the ministry had conceded there were “inconsistencies and contradictions” in the allocation of funding and that is why minister Wissing relieved department head Klaus Bonhoff from his duties.

“The necessary relationship of trust between the minister and the head of department no longer exists.”

Stefan Schnorr, state secretary at the German transportation ministry, in the Frankfurter Allgemeine Zeitung (FAZ)

Furthermore, LobbyControl criticizes what it sees as the inadequacy of compliance rules at the transportation ministry and Bonhoff’s lack of a clear-cut separation between his personal and official contacts when it comes to grant allocation.

Overly cozy network?

Klaus Bonhoff, who is also known as “Mister Hydrogen” due to his extensive experience in leadership roles in the H2 and fuel cell sector, had previously worked for many years on fuel cell cars at Daimler before becoming managing director of Germany’s National Organisation Hydrogen and Fuel Cell Technology, or NOW, in 2008 (see HZwei, April 2011 & H2-international, October 2019). From there he transferred to his post at the German transportation ministry. His successor at NOW since May 2020 has been Kurt-Christoph von Knobelsdorff (see H2-international, February 2021).

Thanks to his considerable expertise, he was a popular and long-standing contributor at numerous industry events since he was well known as an adept public speaker with a skill for highly diplomatic and precise wording. It’s understandable that the DWV in particular wanted to get close to him given that the association comprises many major German industrial corporations from the H2 community and Bonhoff, in his role as NOW spokesman, was the main point of contact for funding applications in the hydrogen sector. However, the responsibility for awarding funds, both then and now, lies with the project management agency Jülich (PtJ).

The DWV’s role

Over the years, the DWV has developed – especially under the leadership of Werner Diwald – from a highly committed body of motivated idealists to an industrial lobbying group. Because of this change, some of the original members who prefer an idealistic approach have turned their back on the association in the past few years. Some of them have urged repeatedly for less dependency on industry and greater levels of transparency. Most recently, Johannes Töpler, who was a long-serving chairman of the DWV, resigned from his post as the DWV’s education officer at the turn of the year. Among the reasons for his resignation was that he no longer thought education and training, a crucial area in his view, was receiving the appropriate attention and appreciation it deserved within the work of the association.

In terms of legal form, the DWV is officially a registered association. Over the years, Diwald has worked to set up various expert commissions to which participating companies pay high-level contributions. This enables the DWV to represent their interests, including on the political stage in Berlin and Brussels. As such, political evenings and business talks are organized on a regular basis where political and industry representatives can meet, as commonly occurs in associations nowadays. One of these expert commissions, HyMobility, was awarded millions of euros in funding in 2021 via the PtJ, i.e., from the transportation ministry’s budget, something which Bonhoff is now being reproached for.

The ministry confirmed to H2-international: “The HyMobility innovation cluster is supported by the Federal Ministry of Transport and Digital Infrastructure as part of the national hydrogen and fuel cell innovation program. The grant is up to €1,438,600. The calculation is based on actual expenditure up to the maximum grant level. […] The HyMobility cluster is financed through grants, contributions for cluster membership, and a proportion of the membership contributions of the DWV. […] The funding project facilitates cluster management, cluster coordination, the support and guidance of the expert commission’s work as well as the preparation of findings from the expert commission and from the expert committees and the provision of recommended courses of action to meet further development needs. In addition, the funding covers the venues for cluster meetings, the creation of studies and analyses as well as technical and legal reports. […] The funding is allocated for specific purposes.”

HyMobility’s aims, according to its project outline, include: “Involvement in the formulation of relevant policy and legal conditions at a national and European level for the market preparation and introduction of low-carbon mobility based on renewable hydrogen. […] the creation and strengthening of understanding for and trust in innovative and low-emission vehicle technology based on renewable hydrogen within transport and national and European politics.”

In connection with this, the DWV confirmed to H2-international that the goals of the expert commissions are to “attract attention for the particular topic, raise awareness, bring together stakeholders from the relevant areas and sectors, prepare joint positions and recommend courses of action to policymakers.

LobbyControl makes the following criticism in relation to this: “It is unusual and questionable that an industrial lobbying association such as the DWV should receive a state subsidy for work that it would carry out regardless: maintaining networks and lobbying.”

“The HyMobility project is supported by the Federal Ministry of Transport and Digital Infrastructure through a total of EUR 1.8 million in funding as part of the national hydrogen and fuel cell innovation program. The funding guidelines are coordinated by NOW GmbH and executed by the project management agency Jülich (PtJ).”

https://dwv-hymobility.de/organisation/

Bonhoff told H2-international: “HyMobility is funded in the same way that the environment ministry funds the HySteel project which was approved prior to HyMobility.” Tagesspiegel Background reported on this very subject on Feb. 7, 2024: “The ministry [German environment ministry; editor’s note] is satisfied with the project. ‘Such networking is effective and successful, is conducive to the sharing of best practice and the establishment of horizontal and vertical partnerships in research, testing and production.’”

Among the 22 members of HyMobility are NOW and H2 Mobility Deutschland. H2 Mobility is a consortium of various automotive, industrial gas and petroleum companies plus an investment fund focused on the construction of hydrogen refueling stations in Germany. Practically every station that is built and managed by this Berlin-based company is subsidized to the tune of nearly 50 percent from European funds or the funds of German central or regional government. One of the three directors is Lorenz Jung (see H2-international, October 2023), who took up the role in April 2023. According to information from LobbyControl, he is the son-in-law of Oliver Weinmann. Jung, whose wife (Weinmann’s daughter) works at NOW in the communications department, has been a manager at the company virtually since its inception.

The roles of Weinmann and Diwald

Weinmann is a founder and board member of what was then the German hydrogen and fuel cell association (see HZwei, October 2010). Born in Hamburg, he had initially worked for city’s electricity company (Hamburgische Electricitäts-Werke or HEW) which was taken over by Swedish corporation Vattenfall Europe when it became the majority shareholder in 2001. Weinmann held the position of managing director at Vattenfall Europe Innovation GmbH from 2010 to July 2023, followed by head of innovation management at Vattenfall Europe AG. From 2020 onward he has also worked in a voluntary capacity as the president of the DWV. In addition, he is chairman of the NOW advisory council, vice chairman of the hydrogen body Wasserstoffgesellschaft Hamburg and holds or has held – according to his own HyAdvice website through which he offers freelance consulting services on matters including funding – further leadership positions at various organizations, among them Hydrogen Europe and the Energy Storage Systems Association or BVES.

Oliver Weinmann at a parliamentary evening in Berlin in 2022

Similar to the way Weinmann operates with his HyAdvice consulting business, Diwald offers his services through PtXSolutions, formerly known as ENCON.Europe. The company is the vehicle through which the DWV chairman provides consultation as a sideline to institutions such as the DWV, Encon Energy EOOD (ENCON subsidiary), Enertrag (former employer), NOW, Performing Energy (DWV think tank) and Vattenfall Europe Innovation. Originally, ENCON.Europe had undertaken some work for the DWV (see H2-international, October 2020). According to a statement by Diwald, ENCON.Europe at the time played a considerable part in increasing the visibility of the DWV without itself appearing in the limelight. He says the company positioned the DWV and the Performing Energy expert commission exclusively as brands in the political sphere and negotiated in the interests of the association. From 2017, the company’s staff included Dennitsa Nozharova, Werner Diwald’s wife, who at the same time also worked for the DWV and is also involved in Encon Energy EOOD.

Fig. 3: Werner Diwald has been DWV chairman since 2014

Performing Energy was the first expert commission that the DWV initiated in 2015 on the back of Warner Diwald’s efforts; Diwald himself had previously created this alliance for wind-based hydrogen systems in 2011 and taken up the position of its speaker (see HZwei, January 2012). Participating organizations include Enertrag and Vattenfall as well as other companies which are also involved in other groups within the network.

Werner Diwald addressed the situation regarding some association members by stating in an email seen by H2-international: “The media’s assumptions about a possible breach by the DWV of compliance rules in relation to the funding application made by the HyMobility innovation cluster are unfounded. […] There was no improper influence exerted by the DWV. The DWV does not accept funding to carry out its statutory activities. […] By virtue of the funding of the HyMobility innovation cluster by the BMDV, the DWV has clearly not placed itself in a position of dependence on the government.”

Furthermore, the DWV has yet to issue a public statement, with the exception of a communication disseminated to association members (as seen by H2-international). The message sent, at the end of February 2024, outlined that “initial measures” have been “immediately introduced” that “go beyond the content of the DWV’s ‘Code of Compliance’ in order to make a comprehensive review of the situation.” It goes on to say that the DWV executive committee has “immediately commissioned a comprehensive review of the DWV’s compliance rules and of external and internal processes and procedures in the context of funding applications and funding allocations.” This is to be carried out by Berlin law office Redeker Sellner Dahs.

H2 funding frozen?

The saga then reached its peak after Der Spiegel reported that the transportation minister had allegedly frozen all funding for H2 projects. According to the article, no more funding is to be approved for the sector for the time being and no further agreements are to be concluded. Even amendment notices will require approval at state secretary level, it said.

However, a press spokeswoman for the ministry clarified the issue at a press conference on Feb. 21, 2024, by stating that the ministry had “not stopped hydrogen funding per se” but is carrying out more thorough assessments of funding applications. These “are currently focused on the approvals procedure for the DWV’s HyMobility funding project.” Should relevant evidence be produced during the investigation, further funding projects will also be examined more closely if necessary.

The reason for this tightened approach seems to be the Brunner affair. It relates, among other things, to the email exchange that took place via a personal GMX account through which Klaus Bonhoff and others communicated with Bavarian businessman Tobias Brunner, managing director of Cryomotive and Hynergy and a key figure in establishing the hydrogen technology application center WTAZ in Pfeffenhausen. LobbyControl disapproves of this “use of a private email account for official communication” since it meant this email exchange was not known to the ministry’s internal review department and therefore could not be taken into consideration in its final report. In all, there are 14 gigabytes of data that require sifting, which explains why there is a delay in the processing of further approvals.

Author: Sven Geitmann

by Hydrogeit | Mar 15, 2024 | Development, Europe, international, News

Fuel Cell Industry Review 2022

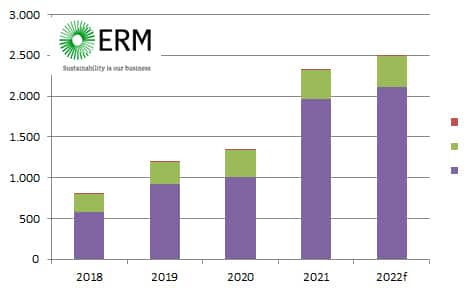

Year 2022 saw fuel cell shipments creep up over 2021 numbers, though the latter was a remarkable year. When 2021 exceeded 2020’s MW numbers by over 70%, we thought we were finally seeing the uptick that had been anticipated – the classic “hockey stick” pattern. But the structure of the industry – and its reliance on only a few players for the majority of shipments – means that growth comes in spurts.

E4tech’s eighth annual Fuel Cell Industry Review showed just under 86,000 units shipped in 2021, or just over 2,300 MW, even with the COVID pandemic still hanging over markets. But this rapid growth was largely due to the activities of two vehicle OEMs, Hyundai and Toyota, together accounting for over 70% of the megawatts. But even after taking these out of the picture, growth continues – slowly but surely.

Advertisements

E4tech is now part of ERM and the team is continuing to research and write the Review. The ninth FCIR shows that 2022 shipments were similar to the year before – with the continued but slow growth still led by Hyundai and Toyota, at over 60% of MW shipments, and by fuel cell buses and trucks into China. In 2022, we estimate nearly 89,200 fuel cells to have been shipped, amounting to almost 2,500 MW.

Analysis by region

For vehicles (which by far is the largest contribution, at 85% of all shipments by megawatts), much of the demand was localized to China and South Korea. China saw over 4,150 units being shipped, across all modes of mobility (including forklifts, now slowly taking off in the country), while South Korea saw nearly 10,400 deployments, dominated by Hyundai’s Nexo. Together with 831 Toyota Mirais going into the home market of Japan, Asia now accounts for around 15,600 units into transportation markets, or 17% of global shipments of fuel cells by number, but rather more impressively some 1,500 MW (60%) of the shipped megawatt count.

Hyundai is benefitting from the 50% subsidy for fuel cell vehicles in South Korea. South Korea is now also the single largest market for large stationary units, in CHP and prime power modes. Stationary shipments into the country grew from 147 MW in 2021 to 196 MW in 2022 (8% of the global MW count). These numbers illustrate the importance of South Korea for fuel cell shipments – and, moreover, the key role of sustained policy and subsidies in helping fuel cell companies and OEMs to achieve volume.

In context of the Japan’s Ene-Farm program, across all markets (stationary, mobility and portable), Asia accounts for 60,850 units (two-thirds of global shipments) and 1,770 MW (71% of global shipments). Behind Asia is North America, with around 14,550 fuel cell shipments (nearly 485 MW, or 19% of global shipments in megawatts), led by Toyota and Bloom Energy shipments to the United States. Europe accounted for roughly 13,250 of fuel cell shipments in 2022, down from just over 14,000 units in 2021. The fall in unit shipments followed the completion of the PACE program of the US Inflation Reduction Act and the imminent closure of KfW-433 grant funding by Germany. In megawatts, the count slightly increased, from a corrected 204 MW in 2021 to 228 MW in 2022, about 9% of the global market. Fuel cell vehicle shipments to Europe are lower than for Asia and the US because of the low subsidies provided by the national governments.

Analysis by application

Fuel cells for mobility, primarily cars, continued to dominate the overall count. Across all modes of mobility (including forklifts), 85% of shipments (2,100 MW) fell into this category in 2022, 150 MW more than in 2021. In units, mobility accounted for 35% of shipments in 2022, a slight fall from 2021’s share. So, the message is transportation is growing, but other fuel cell markets are growing too.

The next main contributor to vehicle shipments is China, with a record 3,789 units (buses and trucks) being shipped over 2022. Together, these are estimated as contributing 387 MW to the overall count in 2022.

While nearly 1,000 fuel cell buses were shipped into China in 2022, fewer came to Europe in 2022 (only 99 registrations). According to CALSTART figures, as many as 82 new fuel cell buses were fielded in the US in 2022, mostly in California. Outside China, fuel cell truck shipments globally in 2022 remained minuscule. This could change, given the business plans of Cellcentric, Plastic Omnium, Hyzon and others.

Fuel cells for ships and for aviation remains exploratory, now with a growing emphasis on propulsion rather than hotel loads or auxiliary power. Forklifts continue to be a major application for fuel cells, albeit with fewer unit shipments in 2022 (over 9,650 units) compared to 2021 (over 13,400 units). Prime power and CHP comprise a large part of the remaining demand, in unit numbers and in MW. By number, micro-CHP still dominates, with Japan leading with its Ene-Farm program. ACE shows 42,877 units being installed in 2022, over 3,000 units more than the previous year. Outside Japan and Europe, micro-CHP shipped in negligible numbers, further demonstrating the criticality of country-to-country policy in supporting fuel cells. Together, prime power and CHP across the power range contributed 364 MW shipments in 2022, up from 335 MW in 2021. Although a growing emphasis for developers, fuel cells for grid support and off-grid power has remained subdued, at 14 MW (for both years). Shipments of portable fuel cells (including smaller ported APUs, less than 20 kW in power output) showed an increase, from just over 6,000 units in 2021 to nearly 8,000 units in 2022. These are supplied globally, but most feed into European and North American industrial and consumer markets.

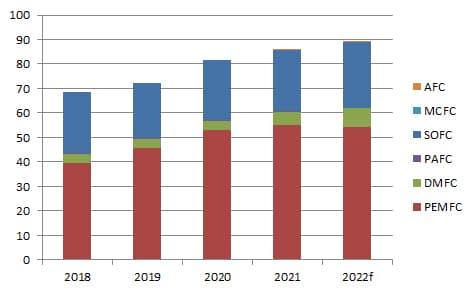

Shipments by fuel cell type

PEM continues to outweigh other fuel cell types in shipments, both in volume and in MW capacity. Of the nearly 90,500 fuel cells shipped in 2022, over 55,000 were PEM. By megawatts, PEM fuel cells recorded 2,151 MW, 86% of the overall volume of shipments.

High-temperature PEM, generally utilizing methanol rather than hydrogen as a fuel, continues to grow, led by Advent Technologies. While still a fraction of overall PEM units at present, shipments are set to grow more aggressively given the improved logistics and increased runtimes enabled by the methanol fuel. DMFC (direct methanol) had a good year, with nearly 8,000 units shipped over 2022, mostly from SFC Energy.

SOFC (solid oxide) grew to nearly 27,000 units in 2022 (mostly micro-CHP, by number). The MW count grew from 207 MW in 2021 to 249 MW in 2022. Much of this is attributable to stronger sales from Bloom Energy. PAFC (phosphoric acid fuel cell) shipments fell, and while no new MCFC (molten carbonate) system placements were recorded over 2022, FuelCell Energy continues to produce significant volumes of stacks, for mid-life refurbishment of systems. AFC (alkaline) shipments increased to over 100 units in 2022, way down on other fuel cell types despite the lower cost potential, both for the fuel cell stack and the hydrogen purity requirement.

Summary

Fuel cells had a good year in 2022. Despite shipments being dominated by a few key suppliers into just a few countries, we are at last beginning to see shipments into Australia and South America, buoyed by the greater interest in hydrogen generally. And while interest is helpful, it remains the case that fuel cells have yet to break through the high capital cost threshold, and (for the hydrogen-fueled units) high fuel prices. We are slowly seeing this happen, through big changes to the supplier landscape, the IPCEI initiative in Europe, significant capacity upgrades to fuel cell production, and the Inflation Reduction Act in the US. But for now, the message remains the same: sustained support from governments is still needed to allow fuel cells to fully support the energy transition. Some fuel cell companies are now also purposing their designs to electrolysis, to help push the market, and with it the hockey stick.

ERM’s Review, a digest of the year’s activity, together with an analysis of fuel cell shipments by region, type and application year on year, is available at http://FuelCellIndustryReview.com. The 2022 edition is delayed, but coming soon. We would like to thank all the fuel cell shippers who graciously provide shipment numbers to us each year, which helps underpin our review.

Author: Stuart Jones, ERM, London, UK, Stuart.Jones@erm.com